<xsd:complexType name="FxFixing">

<xsd:annotation>

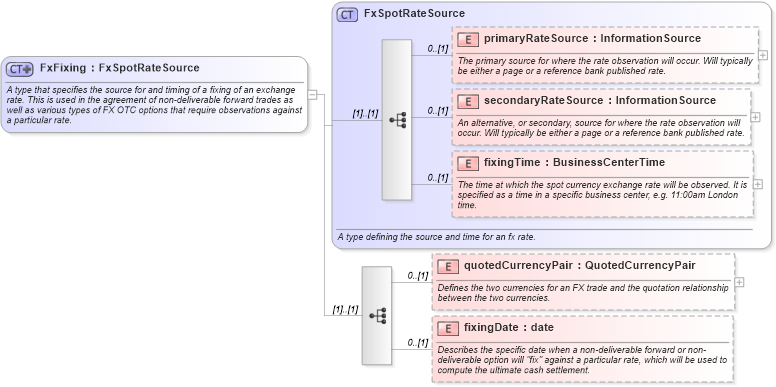

<xsd:documentation xml:lang="en">A type that specifies the source for and timing of a fixing of an exchange rate. This is used in the agreement of non-deliverable forward trades as well as various types of FX OTC options that require observations against a particular rate.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="FxSpotRateSource">

<xsd:sequence>

<xsd:element name="quotedCurrencyPair" type="QuotedCurrencyPair" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the two currencies for an FX trade and the quotation relationship between the two currencies.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="fixingDate" type="xsd:date" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Describes the specific date when a non-deliverable forward or non-deliverable option will "fix" against a particular rate, which will be used to compute the ultimate cash settlement.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|