<xsd:complexType name="FloatingLegCalculation">

<xsd:annotation>

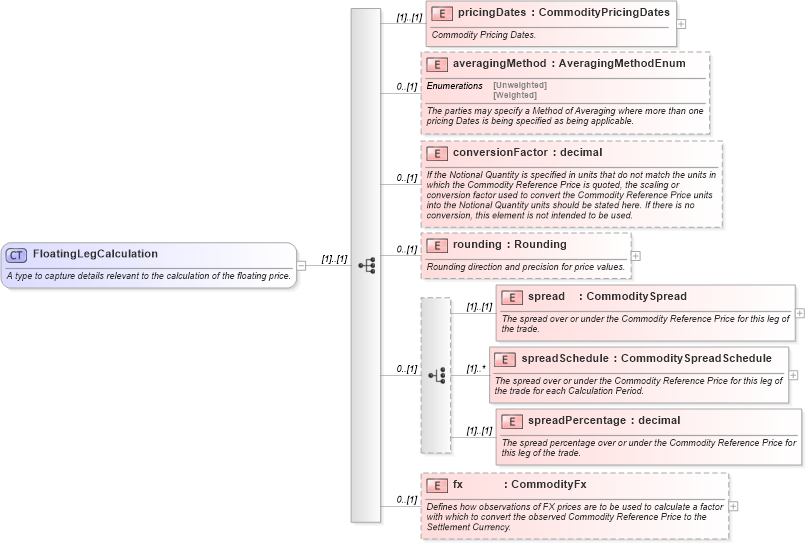

<xsd:documentation xml:lang="en">A type to capture details relevant to the calculation of the floating price.</xsd:documentation>

</xsd:annotation>

<xsd:sequence>

<xsd:element name="pricingDates" type="CommodityPricingDates">

<xsd:annotation>

<xsd:documentation xml:lang="en">Commodity Pricing Dates.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="averagingMethod" type="AveragingMethodEnum" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The parties may specify a Method of Averaging where more than one pricing Dates is being specified as being applicable.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="conversionFactor" type="xsd:decimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">If the Notional Quantity is specified in units that do not match the units in which the Commodity Reference Price is quoted, the scaling or conversion factor used to convert the Commodity Reference Price units into the Notional Quantity units should be stated here. If there is no conversion, this element is not intended to be used.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="rounding" type="Rounding" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Rounding direction and precision for price values.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:choice minOccurs="0">

<xsd:element name="spread" type="CommoditySpread">

<xsd:annotation>

<xsd:documentation xml:lang="en">The spread over or under the Commodity Reference Price for this leg of the trade.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="spreadSchedule" type="CommoditySpreadSchedule" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">The spread over or under the Commodity Reference Price for this leg of the trade for each Calculation Period.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="spreadPercentage" type="xsd:decimal">

<xsd:annotation>

<xsd:documentation xml:lang="en">The spread percentage over or under the Commodity Reference Price for this leg of the trade.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:choice>

<xsd:element name="fx" type="CommodityFx" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines how observations of FX prices are to be used to calculate a factor with which to convert the observed Commodity Reference Price to the Settlement Currency.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:complexType>

|