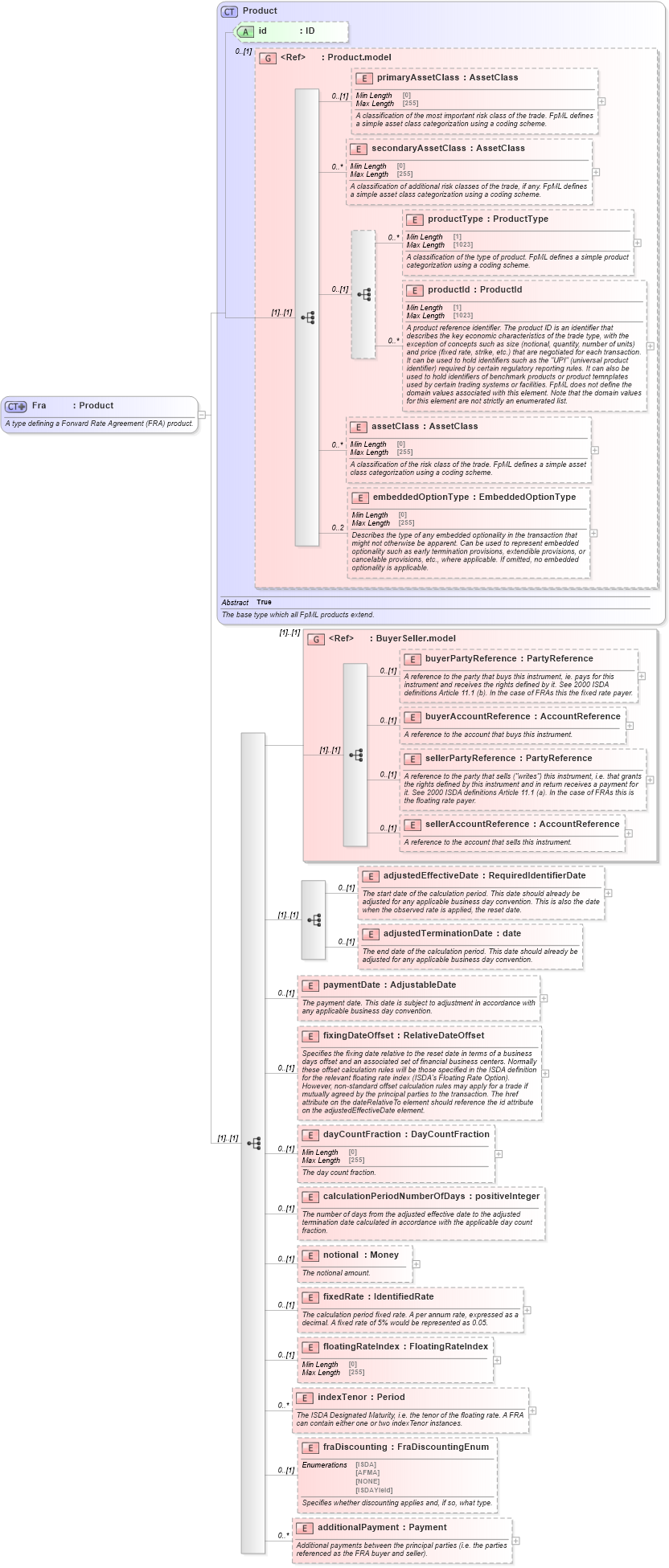

<xsd:complexType name="Fra">

<xsd:annotation>

<xsd:documentation xml:lang="en">A type defining a Forward Rate Agreement (FRA) product.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="Product">

<xsd:sequence>

<xsd:group ref="BuyerSeller.model" />

<xsd:sequence>

<xsd:element name="adjustedEffectiveDate" type="RequiredIdentifierDate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The start date of the calculation period. This date should already be adjusted for any applicable business day convention. This is also the date when the observed rate is applied, the reset date.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="adjustedTerminationDate" type="xsd:date" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The end date of the calculation period. This date should already be adjusted for any applicable business day convention.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

<xsd:element name="paymentDate" type="AdjustableDate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The payment date. This date is subject to adjustment in accordance with any applicable business day convention.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="fixingDateOffset" type="RelativeDateOffset" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the fixing date relative to the reset date in terms of a business days offset and an associated set of financial business centers. Normally these offset calculation rules will be those specified in the ISDA definition for the relevant floating rate index (ISDA's Floating Rate Option). However, non-standard offset calculation rules may apply for a trade if mutually agreed by the principal parties to the transaction. The href attribute on the dateRelativeTo element should reference the id attribute on the adjustedEffectiveDate element.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="dayCountFraction" type="DayCountFraction" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The day count fraction.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="calculationPeriodNumberOfDays" type="xsd:positiveInteger" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The number of days from the adjusted effective date to the adjusted termination date calculated in accordance with the applicable day count fraction.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="notional" type="Money" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The notional amount.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="fixedRate" type="IdentifiedRate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The calculation period fixed rate. A per annum rate, expressed as a decimal. A fixed rate of 5% would be represented as 0.05.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="floatingRateIndex" type="FloatingRateIndex" minOccurs="0" />

<xsd:element name="indexTenor" type="Period" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">The ISDA Designated Maturity, i.e. the tenor of the floating rate. A FRA can contain either one or two indexTenor instances.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="fraDiscounting" type="FraDiscountingEnum" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies whether discounting applies and, if so, what type.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="additionalPayment" type="Payment" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">Additional payments between the principal parties (i.e. the parties referenced as the FRA buyer and seller).</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|