<xsd:element name="futureValueNotional" type="FutureValueAmount" minOccurs="0">

<xsd:annotation>

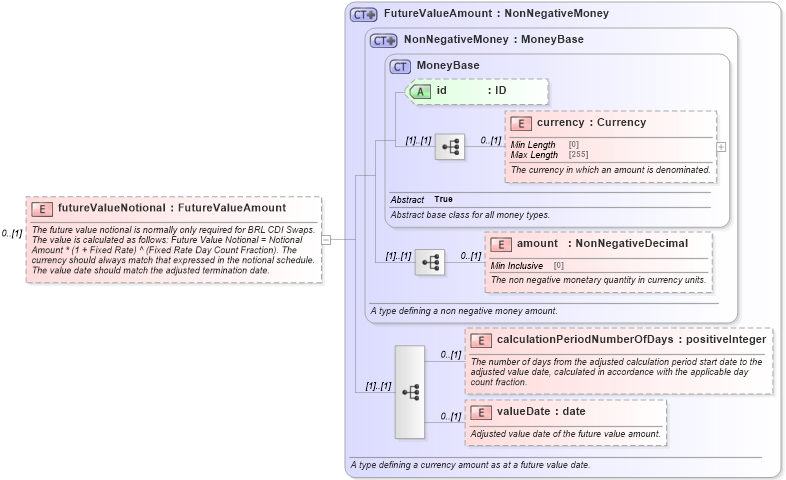

<xsd:documentation xml:lang="en">The future value notional is normally only required for BRL CDI Swaps. The value is calculated as follows: Future Value Notional = Notional Amount * (1 + Fixed Rate) ^ (Fixed Rate Day Count Fraction). The currency should always match that expressed in the notional schedule. The value date should match the adjusted termination date.</xsd:documentation>

</xsd:annotation>

</xsd:element>

|