<xsd:complexType name="FxStraddle">

<xsd:annotation>

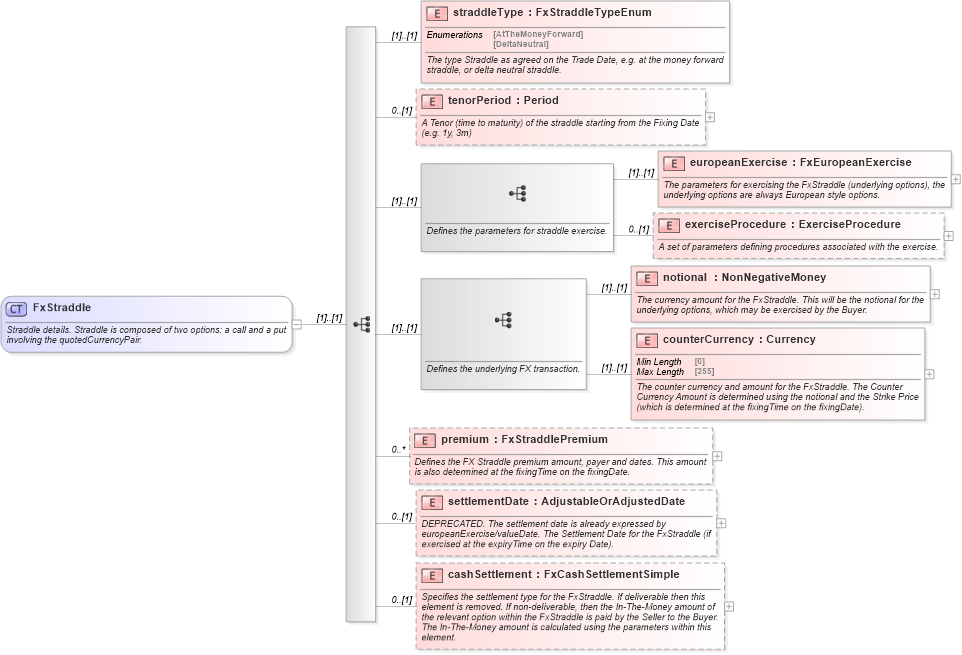

<xsd:documentation xml:lang="en">Straddle details. Straddle is composed of two options: a call and a put involving the quotedCurrencyPair.</xsd:documentation>

</xsd:annotation>

<xsd:sequence>

<xsd:element name="straddleType" type="FxStraddleTypeEnum">

<xsd:annotation>

<xsd:documentation xml:lang="en">The type Straddle as agreed on the Trade Date, e.g. at the money forward straddle, or delta neutral straddle.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="tenorPeriod" type="Period" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">A Tenor (time to maturity) of the straddle starting from the Fixing Date (e.g. 1y, 3m)</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:sequence>

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the parameters for straddle exercise.</xsd:documentation>

</xsd:annotation>

<xsd:element name="europeanExercise" type="FxEuropeanExercise">

<xsd:annotation>

<xsd:documentation xml:lang="en">The parameters for exercising the FxStraddle (underlying options), the underlying options are always European style options.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="exerciseProcedure" type="ExerciseProcedure" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">A set of parameters defining procedures associated with the exercise.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

<xsd:sequence>

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the underlying FX transaction.</xsd:documentation>

</xsd:annotation>

<xsd:element name="notional" type="NonNegativeMoney">

<xsd:annotation>

<xsd:documentation xml:lang="en">The currency amount for the FxStraddle. This will be the notional for the underlying options, which may be exercised by the Buyer.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="counterCurrency" type="Currency">

<xsd:annotation>

<xsd:documentation xml:lang="en">The counter currency and amount for the FxStraddle. The Counter Currency Amount is determined using the notional and the Strike Price (which is determined at the fixingTime on the fixingDate).</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

<xsd:element name="premium" type="FxStraddlePremium" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the FX Straddle premium amount, payer and dates. This amount is also determined at the fixingTime on the fixingDate.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="settlementDate" type="AdjustableOrAdjustedDate" minOccurs="0" fpml-annotation:deprecated="true" fpml-annotation:deprecatedReason="The settlement date is already expressed by europeanExercise/valueDate" xmlns:fpml-annotation="http://www.fpml.org/annotation">

<xsd:annotation>

<xsd:documentation xml:lang="en">DEPRECATED. The settlement date is already expressed by europeanExercise/valueDate. The Settlement Date for the FxStraddle (if exercised at the expiryTime on the expiry Date).</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="cashSettlement" type="FxCashSettlementSimple" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the settlement type for the FxStraddle. If deliverable then this element is removed. If non-deliverable, then the In-The-Money amount of the relevant option within the FxStraddle is paid by the Seller to the Buyer. The In-The-Money amount is calculated using the parameters within this element.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:complexType>

|