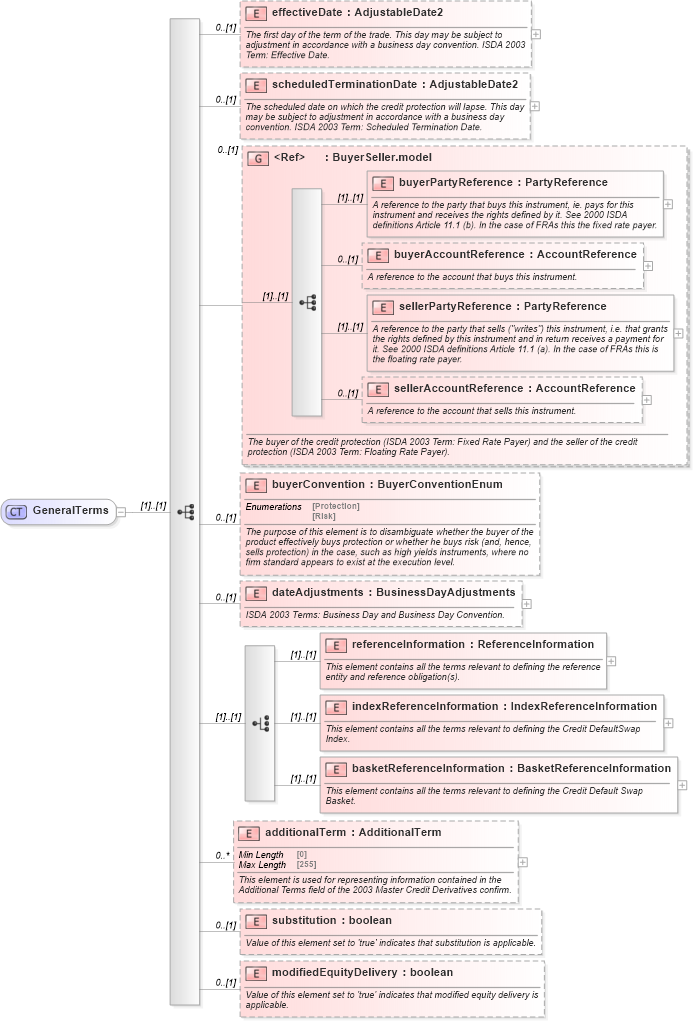

<xsd:complexType name="GeneralTerms">

<xsd:sequence>

<xsd:element name="effectiveDate" type="AdjustableDate2" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The first day of the term of the trade. This day may be subject to adjustment in accordance with a business day convention. ISDA 2003 Term: Effective Date.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="scheduledTerminationDate" type="AdjustableDate2" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The scheduled date on which the credit protection will lapse. This day may be subject to adjustment in accordance with a business day convention. ISDA 2003 Term: Scheduled Termination Date.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:group ref="BuyerSeller.model" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The buyer of the credit protection (ISDA 2003 Term: Fixed Rate Payer) and the seller of the credit protection (ISDA 2003 Term: Floating Rate Payer).</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:element name="buyerConvention" type="BuyerConventionEnum" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The purpose of this element is to disambiguate whether the buyer of the product effectively buys protection or whether he buys risk (and, hence, sells protection) in the case, such as high yields instruments, where no firm standard appears to exist at the execution level.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="dateAdjustments" type="BusinessDayAdjustments" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">ISDA 2003 Terms: Business Day and Business Day Convention.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:choice>

<xsd:element name="referenceInformation" type="ReferenceInformation">

<xsd:annotation>

<xsd:documentation xml:lang="en">This element contains all the terms relevant to defining the reference entity and reference obligation(s).</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="indexReferenceInformation" type="IndexReferenceInformation">

<xsd:annotation>

<xsd:documentation xml:lang="en">This element contains all the terms relevant to defining the Credit DefaultSwap Index.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="basketReferenceInformation" type="BasketReferenceInformation">

<xsd:annotation>

<xsd:documentation xml:lang="en">This element contains all the terms relevant to defining the Credit Default Swap Basket.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:choice>

<xsd:element name="additionalTerm" type="AdditionalTerm" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">This element is used for representing information contained in the Additional Terms field of the 2003 Master Credit Derivatives confirm.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="substitution" type="xsd:boolean" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Value of this element set to 'true' indicates that substitution is applicable.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="modifiedEquityDelivery" type="xsd:boolean" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Value of this element set to 'true' indicates that modified equity delivery is applicable.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:complexType>

|