<xsd:complexType name="InstrumentTradePricing">

<xsd:annotation>

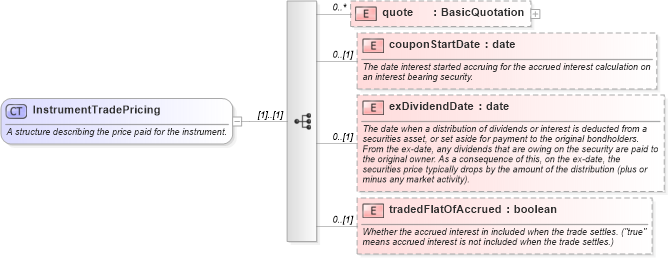

<xsd:documentation xml:lang="en">A structure describing the price paid for the instrument.</xsd:documentation>

</xsd:annotation>

<xsd:sequence>

<xsd:element name="quote" type="BasicQuotation" minOccurs="0" maxOccurs="unbounded" />

<xsd:element name="couponStartDate" type="xsd:date" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The date interest started accruing for the accrued interest calculation on an interest bearing security.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="exDividendDate" type="xsd:date" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The date when a distribution of dividends or interest is deducted from a securities asset, or set aside for payment to the original bondholders. From the ex-date, any dividends that are owing on the security are paid to the original owner. As a consequence of this, on the ex-date, the securities price typically drops by the amount of the distribution (plus or minus any market activity).</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="tradedFlatOfAccrued" type="xsd:boolean" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Whether the accrued interest in included when the trade settles. ("true" means accrued interest is not included when the trade settles.)</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:complexType>

|