<xsd:complexType name="InterestCalculation">

<xsd:annotation>

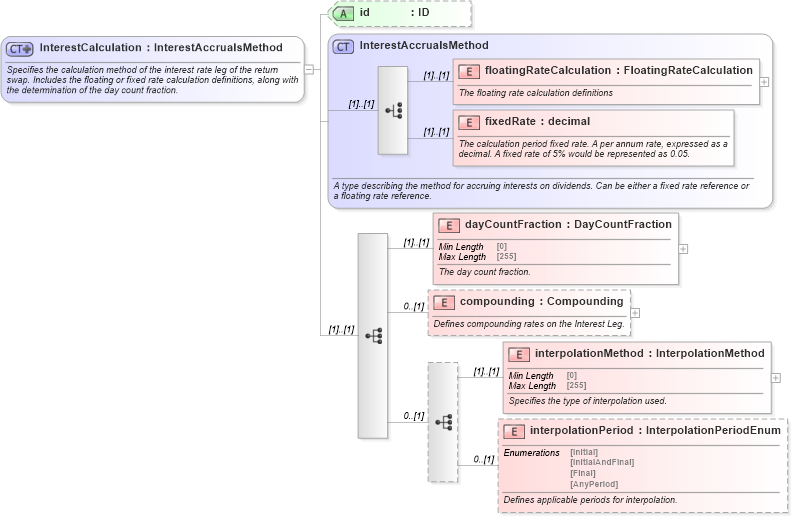

<xsd:documentation xml:lang="en">Specifies the calculation method of the interest rate leg of the return swap. Includes the floating or fixed rate calculation definitions, along with the determination of the day count fraction.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="InterestAccrualsMethod">

<xsd:sequence>

<xsd:element name="dayCountFraction" type="DayCountFraction">

<xsd:annotation>

<xsd:documentation xml:lang="en">The day count fraction.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="compounding" type="Compounding" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines compounding rates on the Interest Leg.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:sequence minOccurs="0">

<xsd:element name="interpolationMethod" type="InterpolationMethod">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the type of interpolation used.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="interpolationPeriod" type="InterpolationPeriodEnum" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines applicable periods for interpolation.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:sequence>

<xsd:attribute name="id" type="xsd:ID" />

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|