| Definition Type: | Element |

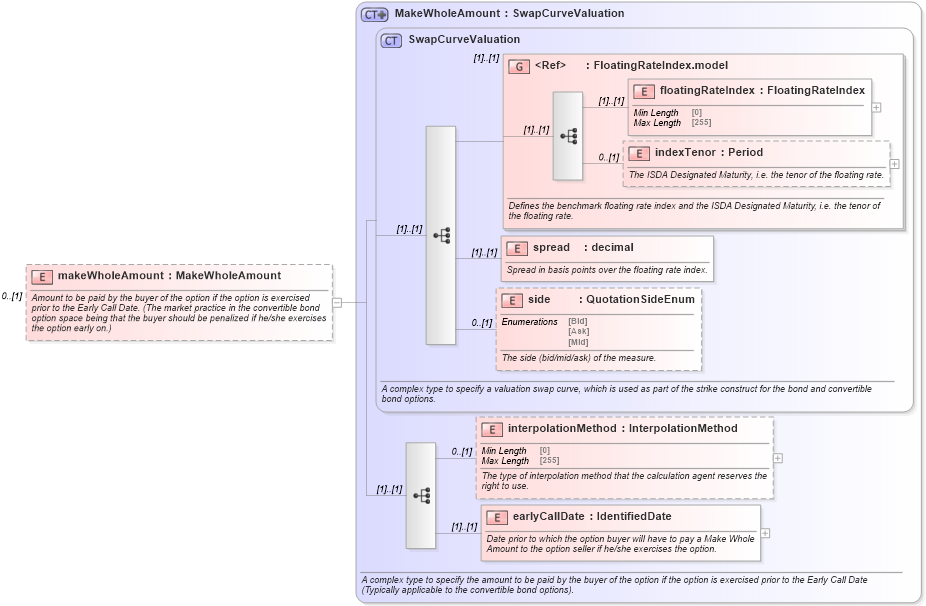

| Name: | makeWholeAmount |

| Namespace: | http://www.fpml.org/FpML-5/confirmation |

| Type: | nsA:MakeWholeAmount |

| Containing Schema: | fpml-bond-option-5-10.xsd |

| MinOccurs | 0 |

| MaxOccurs | (1) |

| Abstract | |

| Documentation: |

Amount to be paid by the buyer of the option if the option is exercised prior to the

Early Call Date. (The market practice in the convertible bond option space being that

the buyer should be penalized if he/she exercises the option early on.)

|

|

|

|

|||||||||||||||||||||||||||||||||

|

|