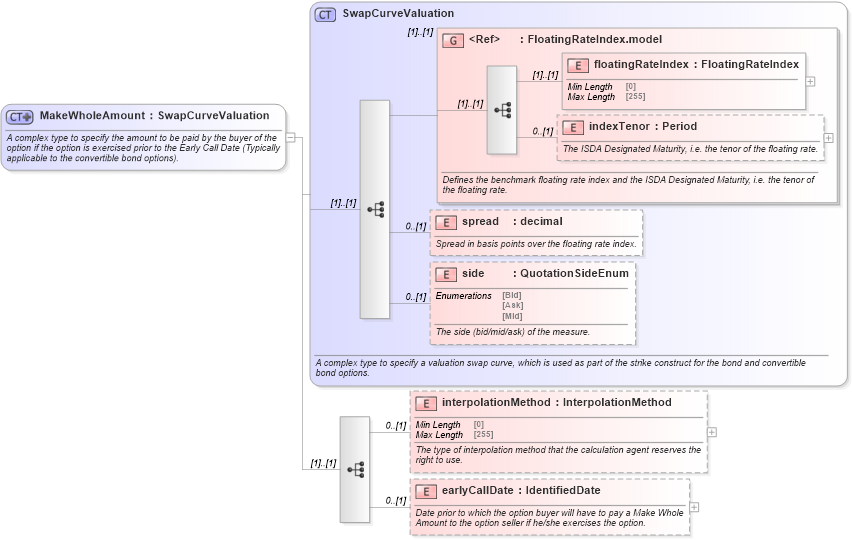

<xsd:complexType name="MakeWholeAmount">

<xsd:annotation>

<xsd:documentation xml:lang="en">A complex type to specify the amount to be paid by the buyer of the option if the option is exercised prior to the Early Call Date (Typically applicable to the convertible bond options).</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="SwapCurveValuation">

<xsd:sequence>

<xsd:element name="interpolationMethod" type="InterpolationMethod" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The type of interpolation method that the calculation agent reserves the right to use.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="earlyCallDate" type="IdentifiedDate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Date prior to which the option buyer will have to pay a Make Whole Amount to the option seller if he/she exercises the option.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|