<xsd:complexType name="SwapCurveValuation">

<xsd:annotation>

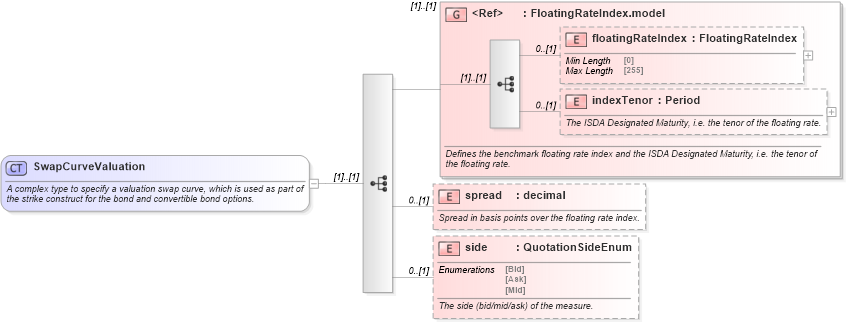

<xsd:documentation xml:lang="en">A complex type to specify a valuation swap curve, which is used as part of the strike construct for the bond and convertible bond options.</xsd:documentation>

</xsd:annotation>

<xsd:sequence>

<xsd:group ref="FloatingRateIndex.model">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the benchmark floating rate index and the ISDA Designated Maturity, i.e. the tenor of the floating rate.</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:element name="spread" type="xsd:decimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Spread in basis points over the floating rate index.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="side" type="QuotationSideEnum" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The side (bid/mid/ask) of the measure.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:complexType>

|