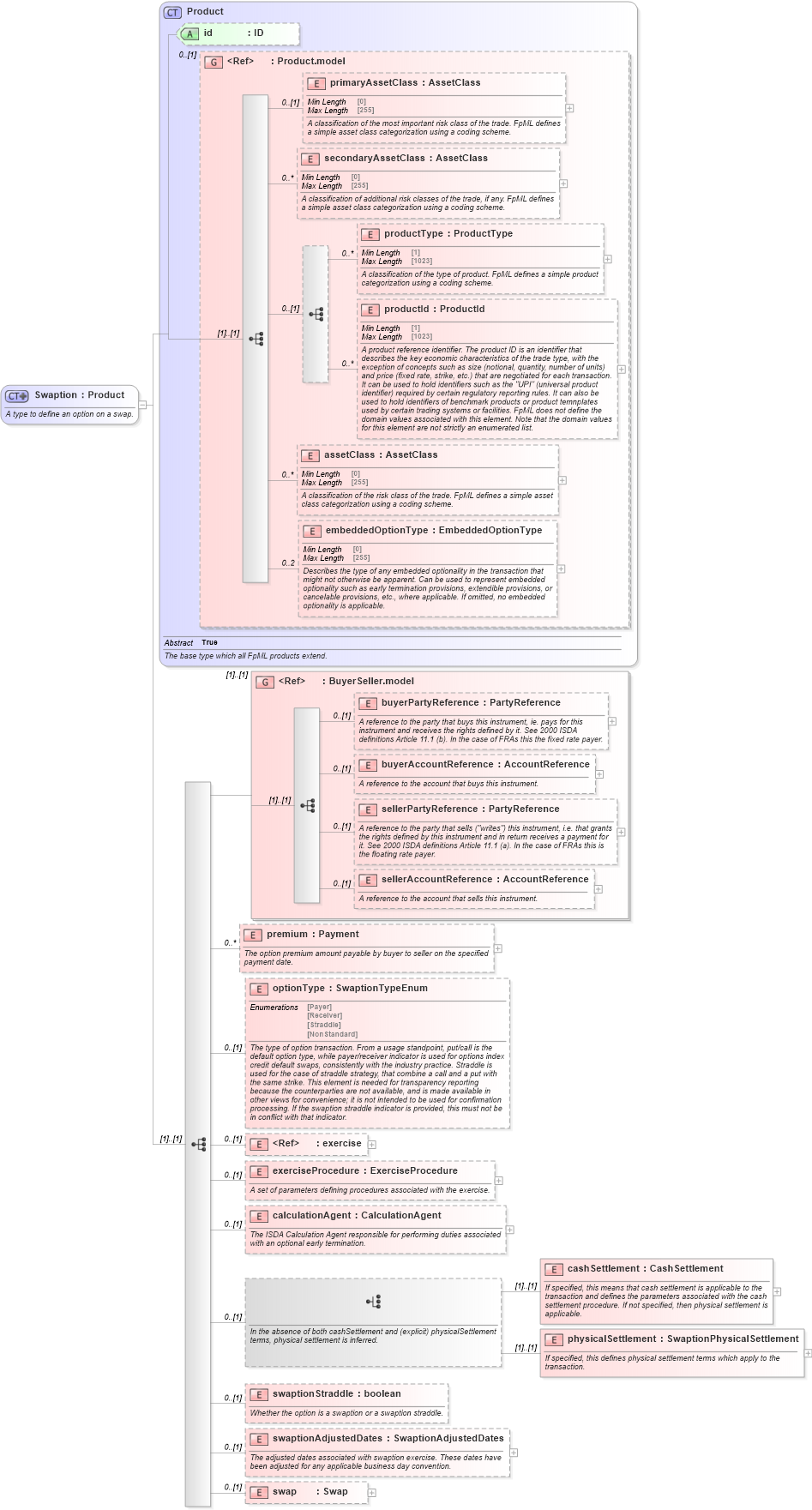

<xsd:complexType name="Swaption">

<xsd:annotation>

<xsd:documentation xml:lang="en">A type to define an option on a swap.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="Product">

<xsd:sequence>

<xsd:group ref="BuyerSeller.model" />

<xsd:element name="premium" type="Payment" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">The option premium amount payable by buyer to seller on the specified payment date.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="optionType" type="SwaptionTypeEnum" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The type of option transaction. From a usage standpoint, put/call is the default option type, while payer/receiver indicator is used for options index credit default swaps, consistently with the industry practice. Straddle is used for the case of straddle strategy, that combine a call and a put with the same strike. This element is needed for transparency reporting because the counterparties are not available, and is made available in other views for convenience; it is not intended to be used for confirmation processing. If the swaption straddle indicator is provided, this must not be in conflict with that indicator.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element ref="exercise" minOccurs="0" />

<xsd:element name="exerciseProcedure" type="ExerciseProcedure" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">A set of parameters defining procedures associated with the exercise.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="calculationAgent" type="CalculationAgent" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The ISDA Calculation Agent responsible for performing duties associated with an optional early termination.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:choice minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">In the absence of both cashSettlement and (explicit) physicalSettlement terms, physical settlement is inferred.</xsd:documentation>

</xsd:annotation>

<xsd:element name="cashSettlement" type="CashSettlement">

<xsd:annotation>

<xsd:documentation xml:lang="en">If specified, this means that cash settlement is applicable to the transaction and defines the parameters associated with the cash settlement procedure. If not specified, then physical settlement is applicable.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="physicalSettlement" type="SwaptionPhysicalSettlement">

<xsd:annotation>

<xsd:documentation xml:lang="en">If specified, this defines physical settlement terms which apply to the transaction.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:choice>

<xsd:element name="swaptionStraddle" type="xsd:boolean" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Whether the option is a swaption or a swaption straddle.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="swaptionAdjustedDates" type="SwaptionAdjustedDates" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The adjusted dates associated with swaption exercise. These dates have been adjusted for any applicable business day convention.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="swap" type="Swap" minOccurs="0" />

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|