| Definition Type: | Element |

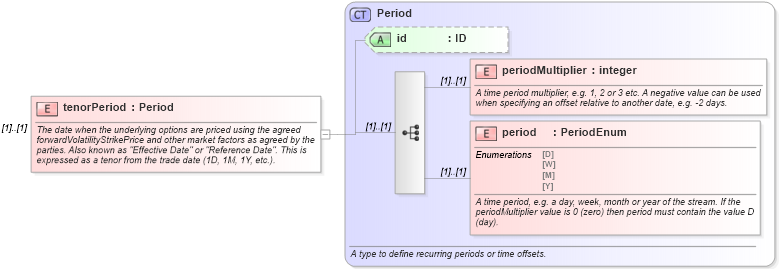

| Name: | tenorPeriod |

| Namespace: | http://www.fpml.org/FpML-5/pretrade |

| Type: | nsC:Period |

| Containing Schema: | fpml-fx-5-10.xsd |

| MinOccurs | (1) |

| MaxOccurs | (1) |

| Abstract | |

| Documentation: |

The date when the underlying options are priced using the agreed forwardVolatilityStrikePrice

and other market factors as agreed by the parties. Also known as "Effective Date"

or "Reference Date". This is expressed as a tenor from the trade date (1D, 1M, 1Y,

etc.).

|

|

|

|

|||||||||||||

|

|||||||||