<xsd:element name="varianceCalculation" type="CommodityVarianceCalculation" minOccurs="0">

<xsd:annotation>

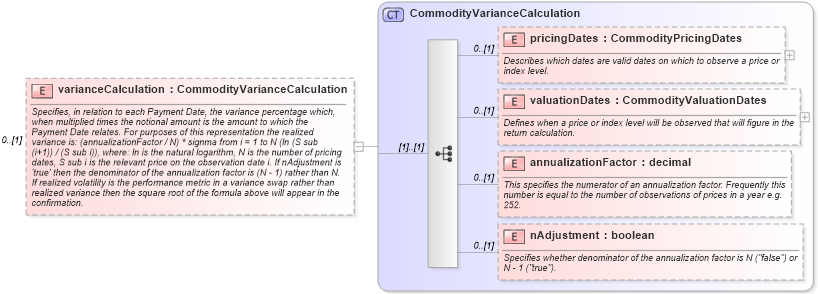

<xsd:documentation xml:lang="en">Specifies, in relation to each Payment Date, the variance percentage which, when multiplied times the notional amount is the amount to which the Payment Date relates. For purposes of this representation the realized variance is: (annualizationFactor / N) * signma from i = 1 to N (ln (S sub (i+1)) / (S sub i)), where: ln is the natural logarithm, N is the number of pricing dates, S sub i is the relevant price on the observation date i. If nAdjustment is 'true' then the denominator of the annualization factor is (N - 1) rather than N. If realized volatility is the performance metric in a variance swap rather than realized variance then the square root of the formula above will appear in the confirmation.</xsd:documentation>

</xsd:annotation>

</xsd:element>

|