<xsd:complexType name="DualCurrencyFeature">

<xsd:annotation>

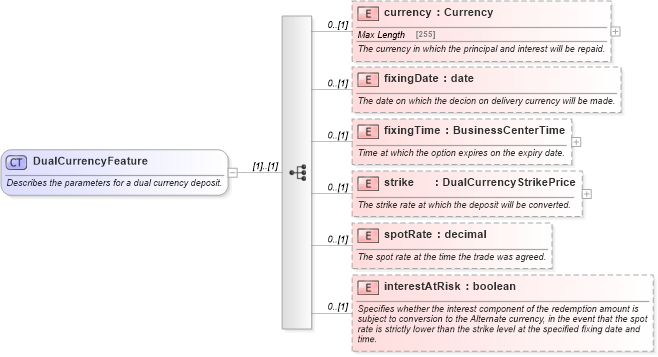

<xsd:documentation xml:lang="en">Describes the parameters for a dual currency deposit.</xsd:documentation>

</xsd:annotation>

<xsd:sequence>

<xsd:element name="currency" type="Currency" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The currency in which the principal and interest will be repaid.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="fixingDate" type="xsd:date" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The date on which the decion on delivery currency will be made.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="fixingTime" type="BusinessCenterTime" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Time at which the option expires on the expiry date.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="strike" type="DualCurrencyStrikePrice" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The strike rate at which the deposit will be converted.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="spotRate" type="xsd:decimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The spot rate at the time the trade was agreed.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="interestAtRisk" type="xsd:boolean" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies whether the interest component of the redemption amount is subject to conversion to the Alternate currency, in the event that the spot rate is strictly lower than the strike level at the specified fixing date and time.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:complexType>

|