<xsd:complexType name="CommodityInterestLeg">

<xsd:annotation>

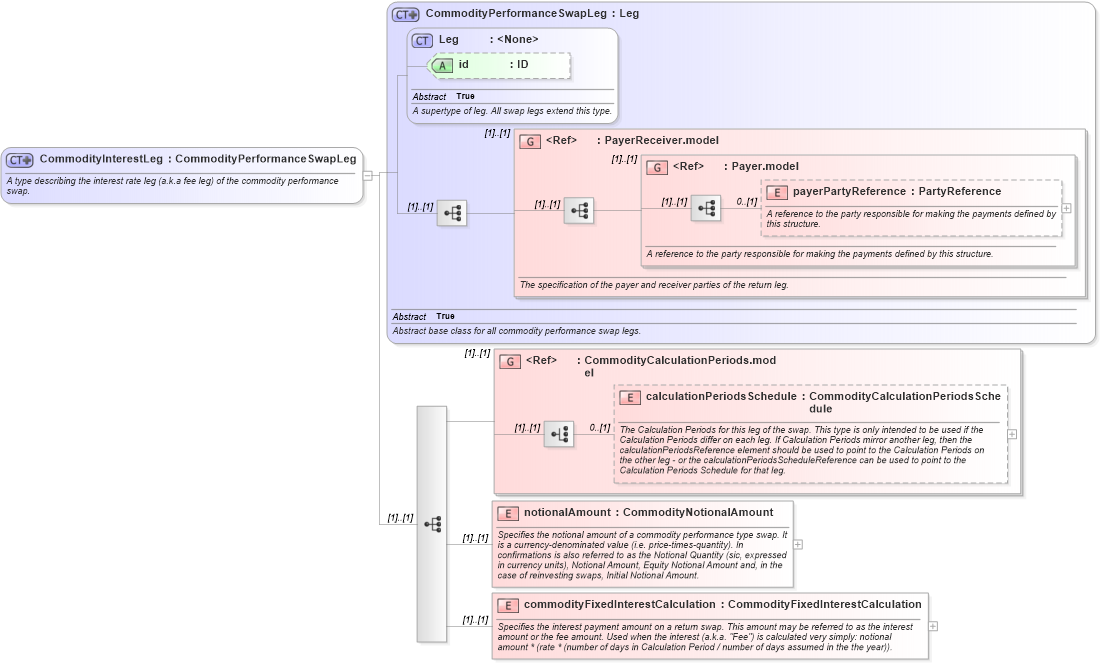

<xsd:documentation xml:lang="en">A type describing the interest rate leg (a.k.a fee leg) of the commodity performance swap.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="CommodityPerformanceSwapLeg">

<xsd:sequence>

<xsd:group ref="CommodityCalculationPeriods.model" />

<!--View Generation: SKIPPED - NonStandardFeature-->

<!--View Generation: Removed a degenerate choice.-->

<xsd:element name="notionalAmount" type="CommodityNotionalAmount">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the notional amount of a commodity performance type swap. It is a currency-denominated value (i.e. price-times-quantity). In confirmations is also referred to as the Notional Quantity (sic, expressed in currency units), Notional Amount, Equity Notional Amount and, in the case of reinvesting swaps, Initial Notional Amount.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<!--In the future this part would be converted into a substitution group with the commodityInterestCalculation as a head of a substitution group. It will be substituted by the commodityFixedInterestCalculation element for fixed interest calculation of the return swap and by other methods of interest calculations, e.g. compounding interest calculation and floating interest calculation -->

<xsd:element name="commodityFixedInterestCalculation" type="CommodityFixedInterestCalculation">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the interest payment amount on a return swap. This amount may be referred to as the interest amount or the fee amount. Used when the interest (a.k.a. "Fee") is calculated very simply: notional amount * (rate * (number of days in Calculation Period / number of days assumed in the the year)).</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|