<xsd:complexType name="FxForwardVolatilityAgreement">

<xsd:annotation>

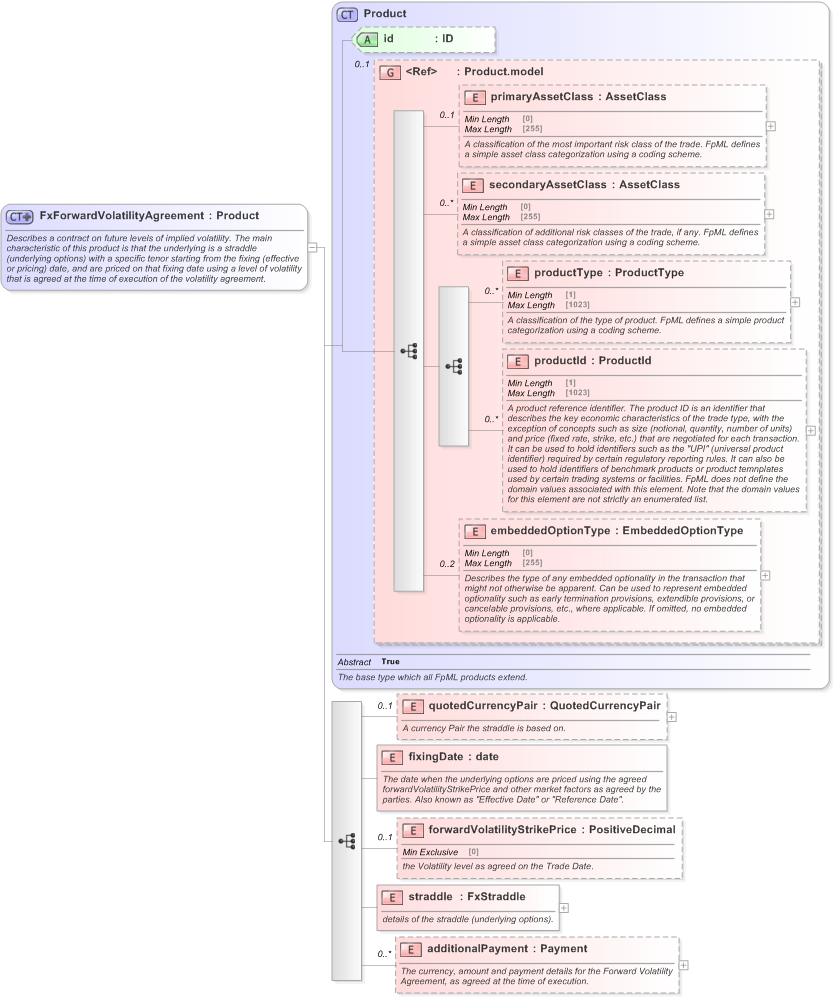

<xsd:documentation xml:lang="en">Describes a contract on future levels of implied volatility. The main characteristic of this product is that the underlying is a straddle (underlying options) with a specific tenor starting from the fixing (effective or pricing) date, and are priced on that fixing date using a level of volatility that is agreed at the time of execution of the volatility agreement.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="Product">

<xsd:sequence>

<xsd:element name="quotedCurrencyPair" type="QuotedCurrencyPair" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">A currency Pair the straddle is based on.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="fixingDate" type="xsd:date">

<xsd:annotation>

<xsd:documentation xml:lang="en">The date when the underlying options are priced using the agreed forwardVolatilityStrikePrice and other market factors as agreed by the parties. Also known as "Effective Date" or "Reference Date".</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="forwardVolatilityStrikePrice" type="PositiveDecimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">the Volatility level as agreed on the Trade Date.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="straddle" type="FxStraddle">

<xsd:annotation>

<xsd:documentation xml:lang="en">details of the straddle (underlying options).</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="additionalPayment" type="Payment" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">The currency, amount and payment details for the Forward Volatility Agreement, as agreed at the time of execution.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|