<xsd:complexType name="Bond">

<xsd:complexContent>

<xsd:extension base="UnderlyingAsset">

<xsd:sequence>

<xsd:element name="relatedExchangeId" type="ExchangeId" minOccurs="0">

<xsd:annotation>

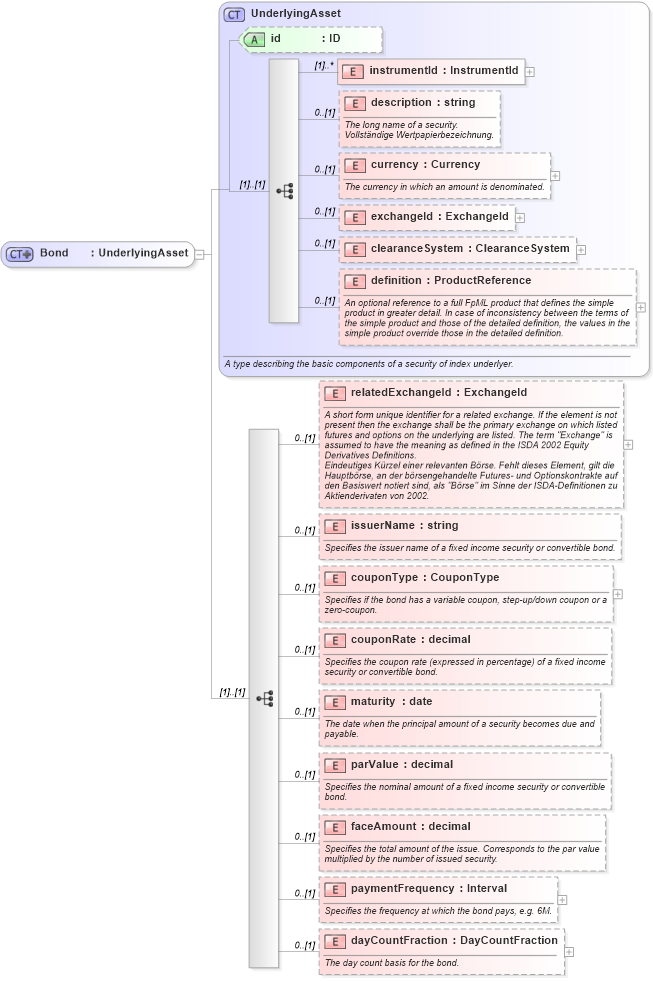

<xsd:documentation xml:lang="en">A short form unique identifier for a related exchange. If the element is not present then the exchange shall be the primary exchange on which listed futures and options on the underlying are listed. The term "Exchange" is assumed to have the meaning as defined in the ISDA 2002 Equity Derivatives Definitions.</xsd:documentation>

<xsd:documentation xml:lang="de">Eindeutiges Kürzel einer relevanten Börse. Fehlt dieses Element, gilt die Hauptbörse, an der börsengehandelte Futures- und Optionskontrakte auf den Basiswert notiert sind, als "Börse" im Sinne der ISDA-Definitionen zu Aktienderivaten von 2002.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="issuerName" type="xsd:string" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the issuer name of a fixed income security or convertible bond.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="couponType" type="CouponType" minOccurs="0">

<xsd:annotation>

<xsd:documentation>Specifies if the bond has a variable coupon, step-up/down coupon or a zero-coupon.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="couponRate" type="xsd:decimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the coupon rate (expressed in percentage) of a fixed income security or convertible bond.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="maturity" type="xsd:date" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The date when the principal amount of a security becomes due and payable.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="parValue" type="xsd:decimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the nominal amount of a fixed income security or convertible bond.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="faceAmount" type="xsd:decimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the total amount of the issue. Corresponds to the par value multiplied by the number of issued security.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="paymentFrequency" type="Interval" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the frequency at which the bond pays, e.g. 6M.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="dayCountFraction" type="DayCountFraction" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The day count basis for the bond.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|