<xsd:complexType name="EquityVarianceAmount">

<xsd:annotation>

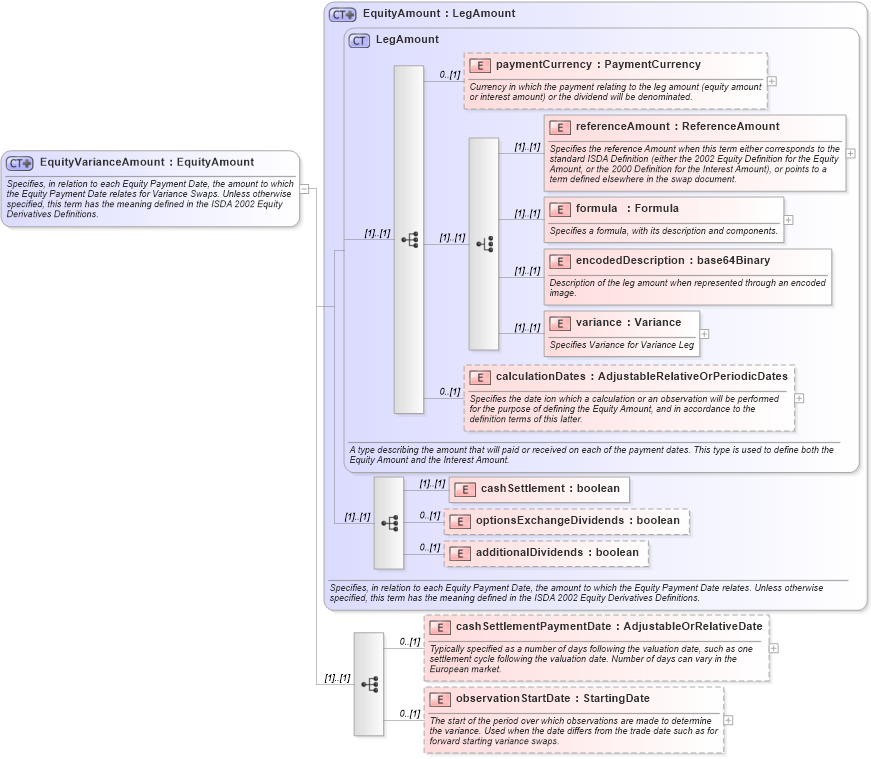

<xsd:documentation xml:lang="en">Specifies, in relation to each Equity Payment Date, the amount to which the Equity Payment Date relates for Variance Swaps. Unless otherwise specified, this term has the meaning defined in the ISDA 2002 Equity Derivatives Definitions.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="EquityAmount">

<xsd:sequence>

<xsd:element name="cashSettlementPaymentDate" type="AdjustableOrRelativeDate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Typically specified as a number of days following the valuation date, such as one settlement cycle following the valuation date. Number of days can vary in the European market.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="observationStartDate" type="StartingDate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The start of the period over which observations are made to determine the variance. Used when the date differs from the trade date such as for forward starting variance swaps.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|