<xsd:complexType name="GeneralTerms">

<xsd:sequence>

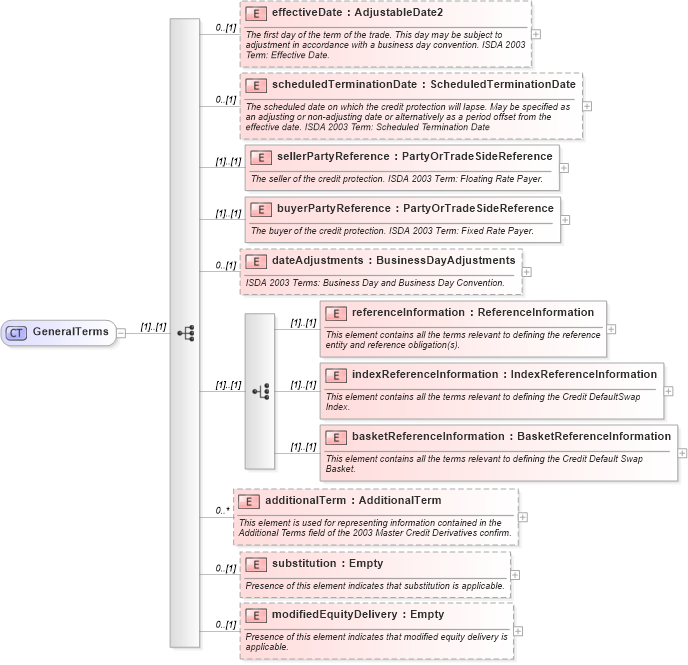

<xsd:element name="effectiveDate" type="AdjustableDate2" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The first day of the term of the trade. This day may be subject to adjustment in accordance with a business day convention. ISDA 2003 Term: Effective Date.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="scheduledTerminationDate" type="ScheduledTerminationDate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The scheduled date on which the credit protection will lapse. May be specified as an adjusting or non-adjusting date or alternatively as a period offset from the effective date. ISDA 2003 Term: Scheduled Termination Date</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="sellerPartyReference" type="PartyOrTradeSideReference">

<xsd:annotation>

<xsd:documentation xml:lang="en">The seller of the credit protection. ISDA 2003 Term: Floating Rate Payer.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="buyerPartyReference" type="PartyOrTradeSideReference">

<xsd:annotation>

<xsd:documentation xml:lang="en">The buyer of the credit protection. ISDA 2003 Term: Fixed Rate Payer.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="dateAdjustments" type="BusinessDayAdjustments" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">ISDA 2003 Terms: Business Day and Business Day Convention.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:choice>

<xsd:element name="referenceInformation" type="ReferenceInformation">

<xsd:annotation>

<xsd:documentation xml:lang="en">This element contains all the terms relevant to defining the reference entity and reference obligation(s).</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="indexReferenceInformation" type="IndexReferenceInformation">

<xsd:annotation>

<xsd:documentation xml:lang="en">This element contains all the terms relevant to defining the Credit DefaultSwap Index.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="basketReferenceInformation" type="BasketReferenceInformation">

<xsd:annotation>

<xsd:documentation xml:lang="en">This element contains all the terms relevant to defining the Credit Default Swap Basket.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:choice>

<xsd:element name="additionalTerm" type="AdditionalTerm" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">This element is used for representing information contained in the Additional Terms field of the 2003 Master Credit Derivatives confirm.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="substitution" type="Empty" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Presence of this element indicates that substitution is applicable.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="modifiedEquityDelivery" type="Empty" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Presence of this element indicates that modified equity delivery is applicable.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:complexType>

|