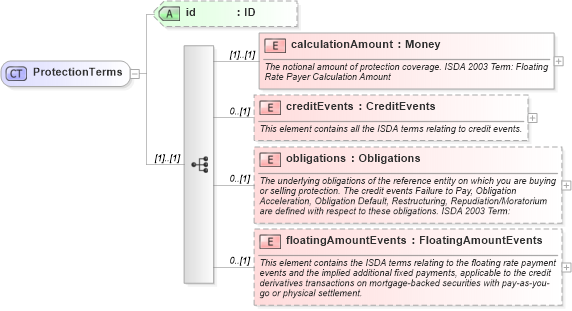

<xsd:complexType name="ProtectionTerms">

<xsd:sequence>

<xsd:element name="calculationAmount" type="Money">

<xsd:annotation>

<xsd:documentation xml:lang="en">The notional amount of protection coverage. ISDA 2003 Term: Floating Rate Payer Calculation Amount</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="creditEvents" type="CreditEvents" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">This element contains all the ISDA terms relating to credit events.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="obligations" type="Obligations" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The underlying obligations of the reference entity on which you are buying or selling protection. The credit events Failure to Pay, Obligation Acceleration, Obligation Default, Restructuring, Repudiation/Moratorium are defined with respect to these obligations. ISDA 2003 Term:</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="floatingAmountEvents" type="FloatingAmountEvents" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">This element contains the ISDA terms relating to the floating rate payment events and the implied additional fixed payments, applicable to the credit derivatives transactions on mortgage-backed securities with pay-as-you-go or physical settlement.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

<xsd:attribute name="id" type="xsd:ID" use="optional" />

</xsd:complexType>

|