<xsd:complexType name="CommodityPricingDates">

<xsd:annotation>

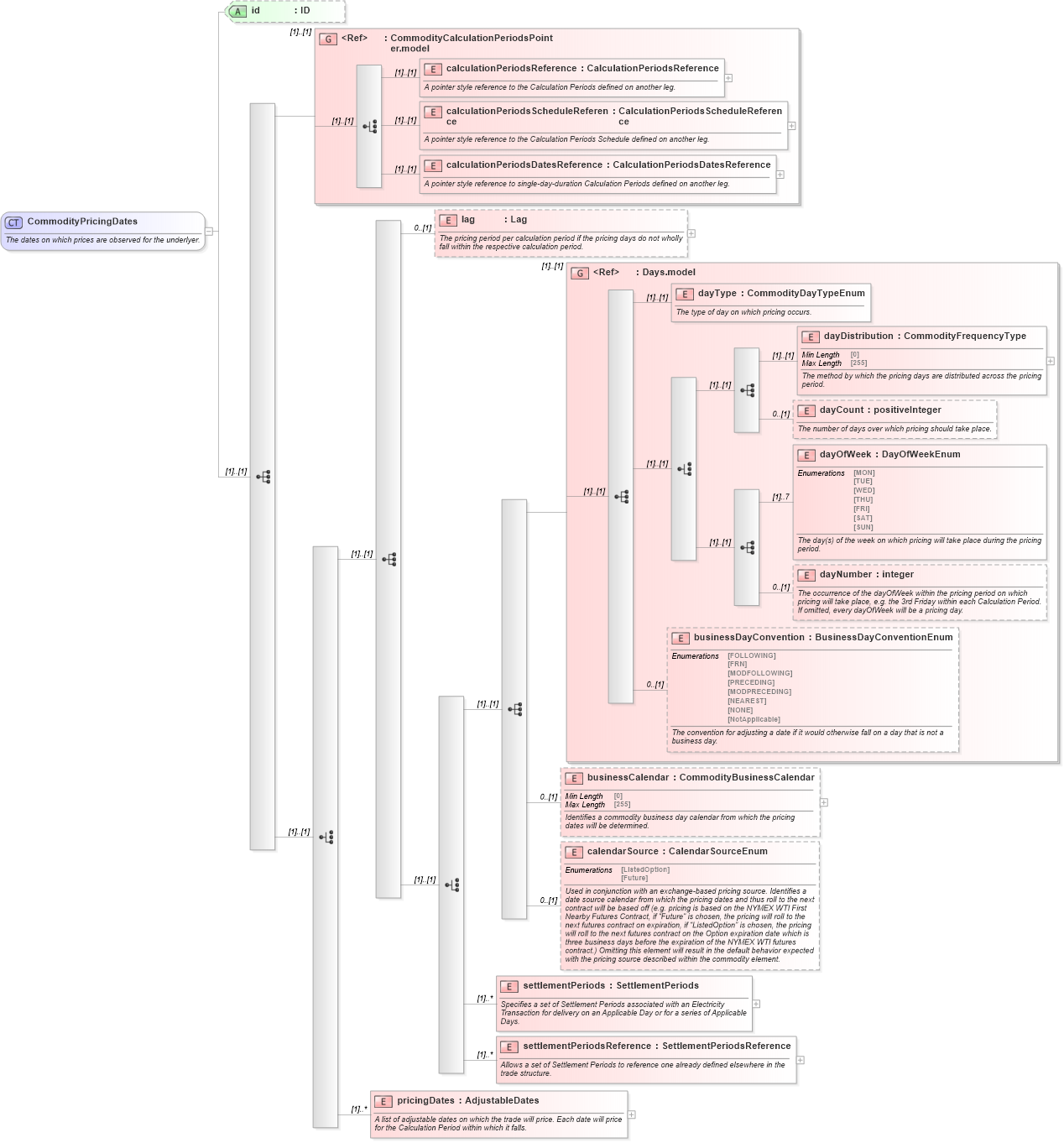

<xsd:documentation xml:lang="en">The dates on which prices are observed for the underlyer.</xsd:documentation>

</xsd:annotation>

<xsd:sequence>

<xsd:group ref="CommodityCalculationPeriodsPointer.model" />

<xsd:choice>

<xsd:sequence>

<xsd:element name="lag" type="Lag" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The pricing period per calculation period if the pricing days do not wholly fall within the respective calculation period.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:choice>

<xsd:sequence>

<xsd:group ref="Days.model" />

<xsd:element name="businessCalendar" type="CommodityBusinessCalendar" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Identifies a commodity business day calendar from which the pricing dates will be determined.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="calendarSource" type="CalendarSourceEnum" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Used in conjunction with an exchange-based pricing source. Identifies a date source calendar from which the pricing dates and thus roll to the next contract will be based off (e.g. pricing is based on the NYMEX WTI First Nearby Futures Contract, if “Future” is chosen, the pricing will roll to the next futures contract on expiration, if “ListedOption” is chosen, the pricing will roll to the next futures contract on the Option expiration date which is three business days before the expiration of the NYMEX WTI futures contract.) Omitting this element will result in the default behavior expected with the pricing source described within the commodity element.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

<xsd:element name="settlementPeriods" type="SettlementPeriods" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies a set of Settlement Periods associated with an Electricity Transaction for delivery on an Applicable Day or for a series of Applicable Days.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="settlementPeriodsReference" type="SettlementPeriodsReference" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">Allows a set of Settlement Periods to reference one already defined elsewhere in the trade structure.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:choice>

</xsd:sequence>

<xsd:element name="pricingDates" type="AdjustableDates" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">A list of adjustable dates on which the trade will price. Each date will price for the Calculation Period within which it falls.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:choice>

</xsd:sequence>

<xsd:attribute name="id" type="xsd:ID" />

</xsd:complexType>

|