<xsd:complexType name="FxAccrualForward">

<xsd:annotation>

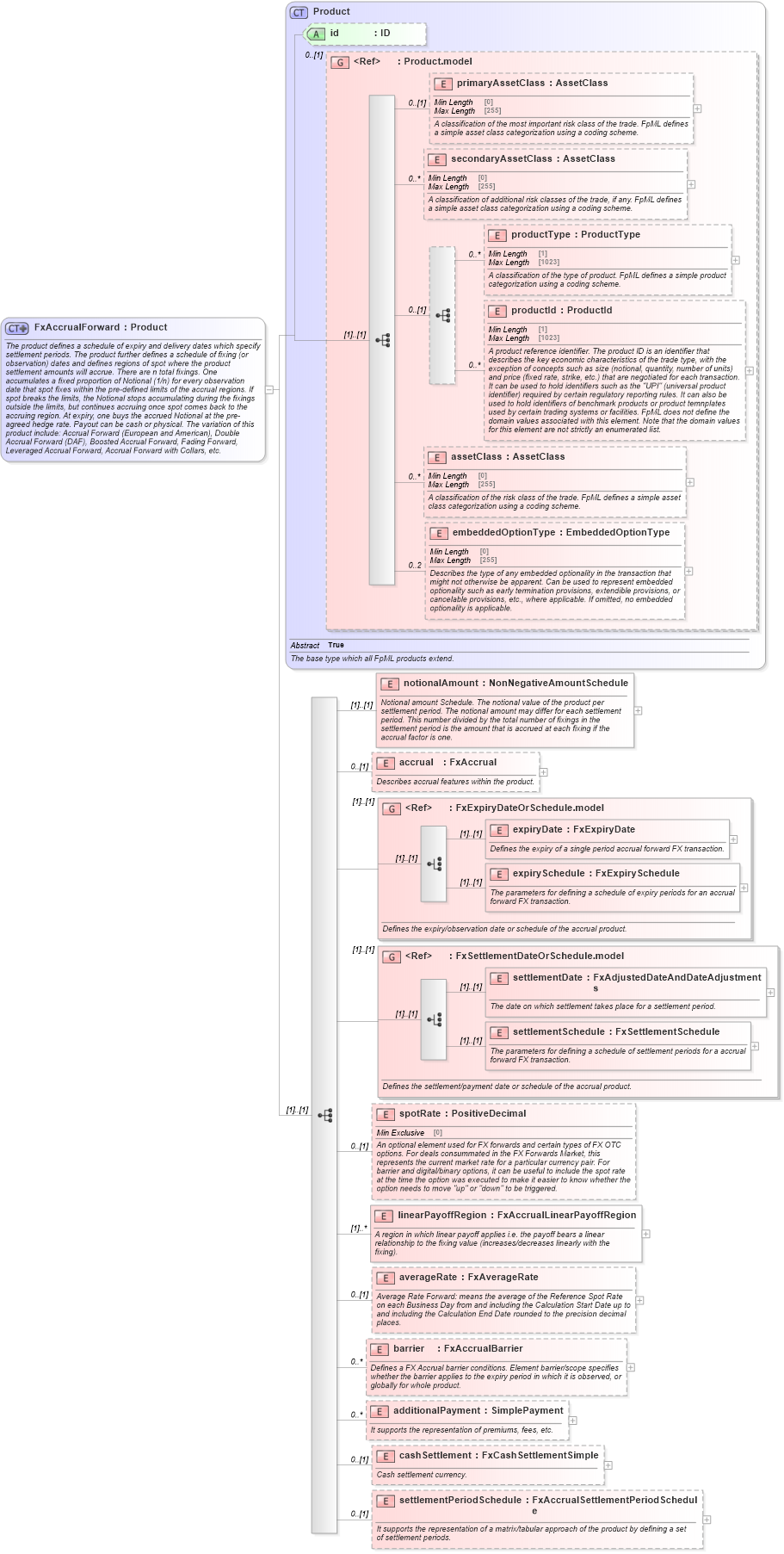

<xsd:documentation xml:lang="en">The product defines a schedule of expiry and delivery dates which specify settlement periods. The product further defines a schedule of fixing (or observation) dates and defines regions of spot where the product settlement amounts will accrue. There are n total fixings. One accumulates a fixed proportion of Notional (1/n) for every observation date that spot fixes within the pre-defined limits of the accrual regions. If spot breaks the limits, the Notional stops accumulating during the fixings outside the limits, but continues accruing once spot comes back to the accruing region. At expiry, one buys the accrued Notional at the pre-agreed hedge rate. Payout can be cash or physical. The variation of this product include: Accrual Forward (European and American), Double Accrual Forward (DAF), Boosted Accrual Forward, Fading Forward, Leveraged Accrual Forward, Accrual Forward with Collars, etc.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="Product">

<xsd:sequence>

<xsd:element name="notionalAmount" type="NonNegativeAmountSchedule">

<xsd:annotation>

<xsd:documentation xml:lang="en">Notional amount Schedule. The notional value of the product per settlement period. The notional amount may differ for each settlement period. This number divided by the total number of fixings in the settlement period is the amount that is accrued at each fixing if the accrual factor is one.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="accrual" type="FxAccrual" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Describes accrual features within the product.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:group ref="FxExpiryDateOrSchedule.model">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the expiry/observation date or schedule of the accrual product.</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:group ref="FxSettlementDateOrSchedule.model">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the settlement/payment date or schedule of the accrual product.</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:element name="spotRate" type="PositiveDecimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">An optional element used for FX forwards and certain types of FX OTC options. For deals consummated in the FX Forwards Market, this represents the current market rate for a particular currency pair. For barrier and digital/binary options, it can be useful to include the spot rate at the time the option was executed to make it easier to know whether the option needs to move "up" or "down" to be triggered.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="linearPayoffRegion" type="FxAccrualLinearPayoffRegion" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">A region in which linear payoff applies i.e. the payoff bears a linear relationship to the fixing value (increases/decreases linearly with the fixing).</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="averageRate" type="FxAverageRate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Average Rate Forward: means the average of the Reference Spot Rate on each Business Day from and including the Calculation Start Date up to and including the Calculation End Date rounded to the precision decimal places.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="barrier" type="FxAccrualBarrier" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines a FX Accrual barrier conditions. Element barrier/scope specifies whether the barrier applies to the expiry period in which it is observed, or globally for whole product.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="additionalPayment" type="SimplePayment" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">It supports the representation of premiums, fees, etc.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="cashSettlement" type="FxCashSettlementSimple" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Cash settlement currency.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="settlementPeriodSchedule" type="FxAccrualSettlementPeriodSchedule" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">It supports the representation of a matrix/tabular approach of the product by defining a set of settlement periods.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|