<xsd:complexType name="FxAccrualOption">

<xsd:annotation>

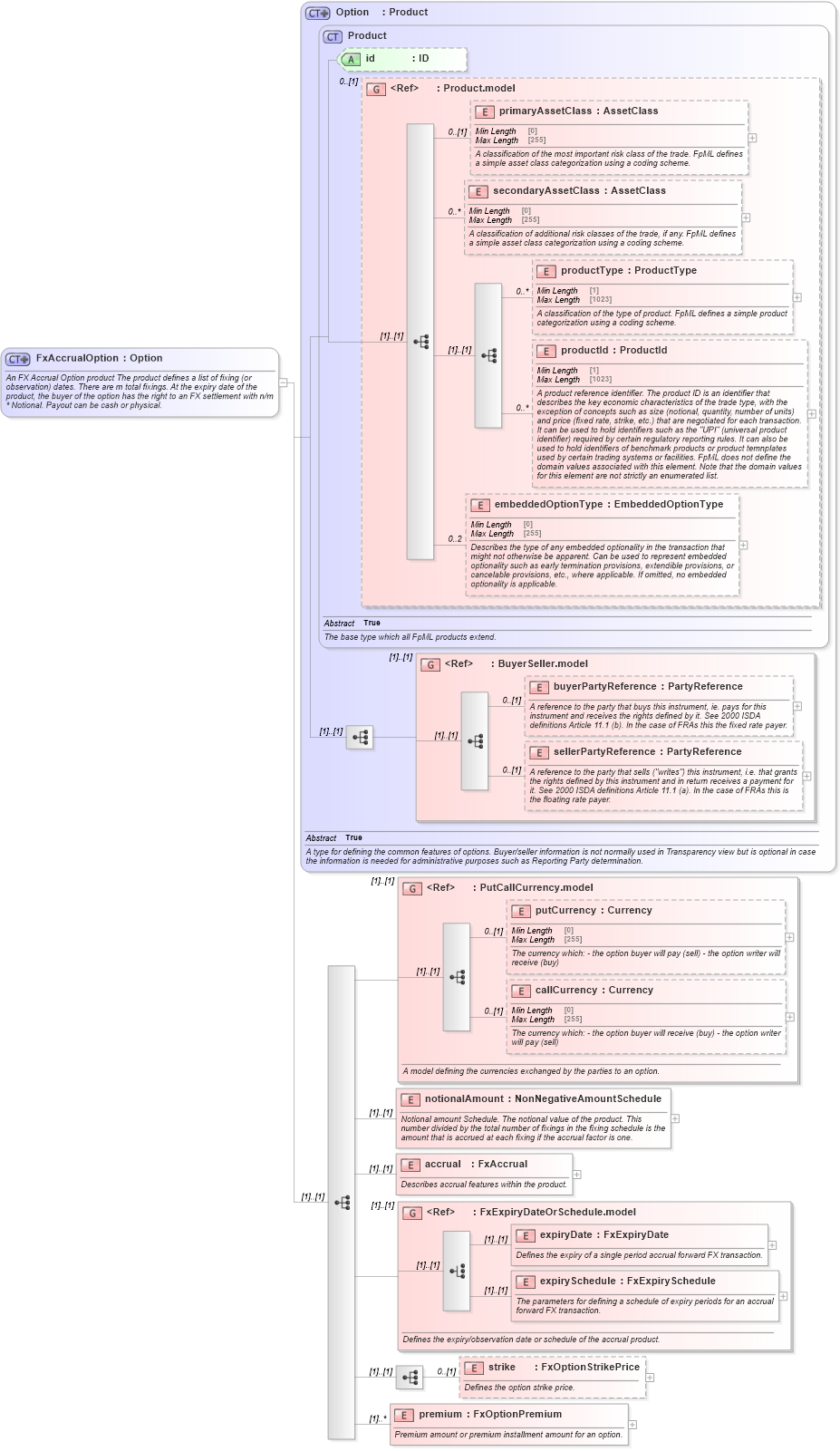

<xsd:documentation xml:lang="en">An FX Accrual Option product The product defines a list of fixing (or observation) dates. There are m total fixings. At the expiry date of the product, the buyer of the option has the right to an FX settlement with n/m * Notional. Payout can be cash or physical.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="Option">

<xsd:sequence>

<xsd:group ref="PutCallCurrency.model">

<xsd:annotation>

<xsd:documentation xml:lang="en">A model defining the currencies exchanged by the parties to an option.</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:element name="notionalAmount" type="NonNegativeAmountSchedule">

<xsd:annotation>

<xsd:documentation xml:lang="en">Notional amount Schedule. The notional value of the product. This number divided by the total number of fixings in the fixing schedule is the amount that is accrued at each fixing if the accrual factor is one.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="accrual" type="FxAccrual">

<xsd:annotation>

<xsd:documentation xml:lang="en">Describes accrual features within the product.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:group ref="FxExpiryDateOrSchedule.model">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the expiry/observation date or schedule of the accrual product.</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:sequence>

<xsd:element name="strike" type="FxOptionStrikePrice" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the option strike price.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

<xsd:element name="premium" type="FxOptionPremium" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">Premium amount or premium installment amount for an option.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|