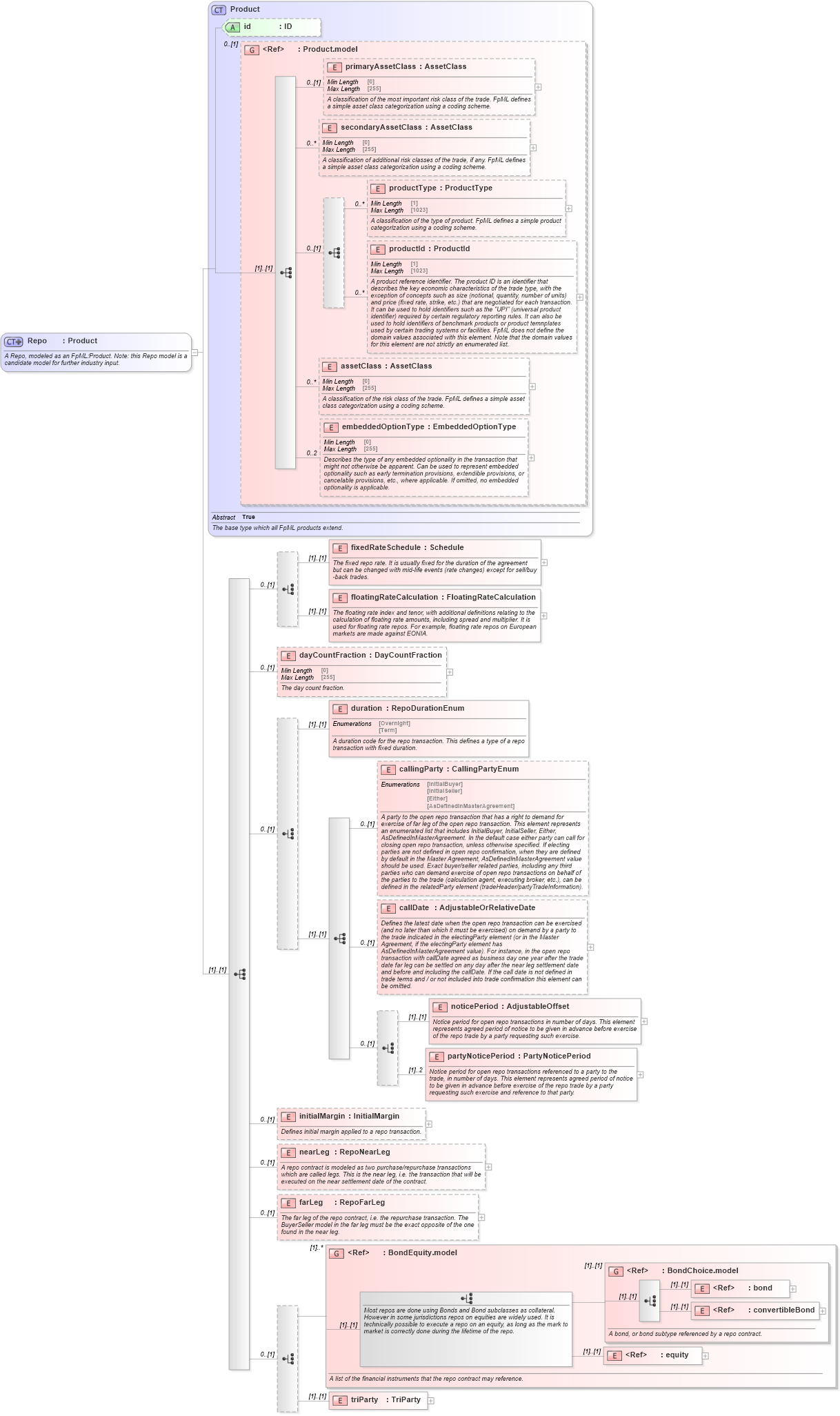

<xsd:complexType name="Repo">

<xsd:annotation>

<xsd:documentation xml:lang="en">A Repo, modeled as an FpML:Product. Note: this Repo model is a candidate model for further industry input.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="Product">

<xsd:sequence>

<xsd:choice minOccurs="0">

<xsd:element name="fixedRateSchedule" type="Schedule">

<xsd:annotation>

<xsd:documentation xml:lang="en">The fixed repo rate. It is usually fixed for the duration of the agreement but can be changed with mid-life events (rate changes) except for sell/buy-back trades.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="floatingRateCalculation" type="FloatingRateCalculation">

<xsd:annotation>

<xsd:documentation xml:lang="en">The floating rate index and tenor, with additional definitions relating to the calculation of floating rate amounts, including spread and multiplier. It is used for floating rate repos. For example, floating rate repos on European markets are made against EONIA.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:choice>

<xsd:element name="dayCountFraction" type="DayCountFraction" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The day count fraction.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:choice minOccurs="0">

<xsd:element name="duration" type="RepoDurationEnum">

<xsd:annotation>

<xsd:documentation xml:lang="en">A duration code for the repo transaction. This defines a type of a repo transaction with fixed duration.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:sequence>

<xsd:element name="callingParty" type="CallingPartyEnum" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">A party to the open repo transaction that has a right to demand for exercise of far leg of the open repo transaction. This element represents an enumerated list that includes InitialBuyer, InitialSeller, Either, AsDefinedInMasterAgreement. In the default case either party can call for closing open repo transaction, unless otherwise specified. If electing parties are not defined in open repo confirmation, when they are defined by default in the Master Agreement, AsDefinedInMasterAgreement value should be used. Exact buyer/seller related parties, including any third parties who can demand exercise of open repo transactions on behalf of the parties to the trade (calculation agent, executing broker, etc.), can be defined in the relatedParty element (tradeHeader/partyTradeInformation).</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="callDate" type="AdjustableOrRelativeDate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the latest date when the open repo transaction can be exercised (and no later than which it must be exercised) on demand by a party to the trade indicated in the electingParty element (or in the Master Agreement, if the electingParty element has AsDefinedInMasterAgreement value). For instance, in the open repo transaction with callDate agreed as business day one year after the trade date far leg can be settled on any day after the near leg settlement date and before and including the callDate. If the call date is not defined in trade terms and / or not included into trade confirmation this element can be omitted.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:choice minOccurs="0">

<xsd:element name="noticePeriod" type="AdjustableOffset">

<xsd:annotation>

<xsd:documentation xml:lang="en">Notice period for open repo transactions in number of days. This element represents agreed period of notice to be given in advance before exercise of the repo trade by a party requesting such exercise.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="partyNoticePeriod" type="PartyNoticePeriod" maxOccurs="2">

<xsd:annotation>

<xsd:documentation xml:lang="en">Notice period for open repo transactions referenced to a party to the trade, in number of days. This element represents agreed period of notice to be given in advance before exercise of the repo trade by a party requesting such exercise and reference to that party.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:choice>

</xsd:sequence>

</xsd:choice>

<xsd:element name="initialMargin" type="InitialMargin" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines initial margin applied to a repo transaction.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="nearLeg" type="RepoNearLeg" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">A repo contract is modeled as two purchase/repurchase transactions which are called legs. This is the near leg, i.e. the transaction that will be executed on the near settlement date of the contract.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="farLeg" type="RepoFarLeg" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The far leg of the repo contract, i.e. the repurchase transaction. The BuyerSeller model in the far leg must be the exact opposite of the one found in the near leg.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:choice minOccurs="0">

<xsd:group ref="BondEquity.model" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">A list of the financial instruments that the repo contract may reference.</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:element name="triParty" type="TriParty" />

</xsd:choice>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|