<xsd:complexType name="ReturnLegValuation">

<xsd:annotation>

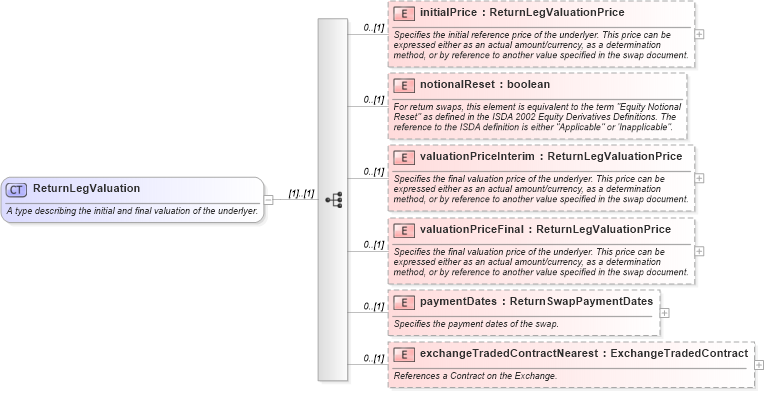

<xsd:documentation xml:lang="en">A type describing the initial and final valuation of the underlyer.</xsd:documentation>

</xsd:annotation>

<xsd:sequence>

<xsd:element name="initialPrice" type="ReturnLegValuationPrice" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the initial reference price of the underlyer. This price can be expressed either as an actual amount/currency, as a determination method, or by reference to another value specified in the swap document.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="notionalReset" type="xsd:boolean" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">For return swaps, this element is equivalent to the term "Equity Notional Reset" as defined in the ISDA 2002 Equity Derivatives Definitions. The reference to the ISDA definition is either "Applicable" or 'Inapplicable".</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="valuationPriceInterim" type="ReturnLegValuationPrice" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the final valuation price of the underlyer. This price can be expressed either as an actual amount/currency, as a determination method, or by reference to another value specified in the swap document.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="valuationPriceFinal" type="ReturnLegValuationPrice" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the final valuation price of the underlyer. This price can be expressed either as an actual amount/currency, as a determination method, or by reference to another value specified in the swap document.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="paymentDates" type="ReturnSwapPaymentDates" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the payment dates of the swap.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="exchangeTradedContractNearest" type="ExchangeTradedContract" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">References a Contract on the Exchange.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:complexType>

|