<xsd:complexType name="UnderlyerInterestLeg">

<xsd:annotation>

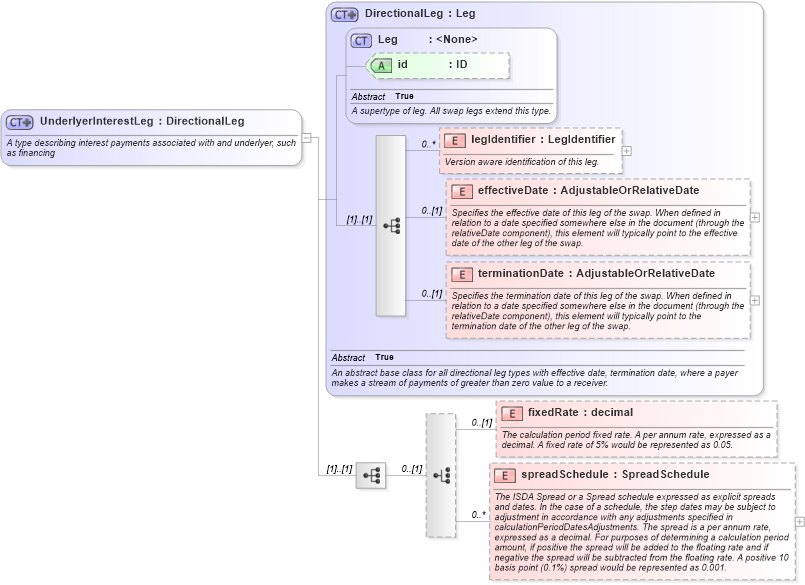

<xsd:documentation xml:lang="en">A type describing interest payments associated with and underlyer, such as financing</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="DirectionalLeg">

<xsd:sequence>

<xsd:choice minOccurs="0">

<xsd:element name="fixedRate" type="xsd:decimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The calculation period fixed rate. A per annum rate, expressed as a decimal. A fixed rate of 5% would be represented as 0.05.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="spreadSchedule" type="SpreadSchedule" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">The ISDA Spread or a Spread schedule expressed as explicit spreads and dates. In the case of a schedule, the step dates may be subject to adjustment in accordance with any adjustments specified in calculationPeriodDatesAdjustments. The spread is a per annum rate, expressed as a decimal. For purposes of determining a calculation period amount, if positive the spread will be added to the floating rate and if negative the spread will be subtracted from the floating rate. A positive 10 basis point (0.1%) spread would be represented as 0.001.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:choice>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|