<xsd:complexType name="DeprecatedVariance" fpml-annotation:deprecated="true" fpml-annotation:deprecatedReason="Use new Variance complex type" xmlns:fpml-annotation="http://www.fpml.org/annotation">

<xsd:annotation>

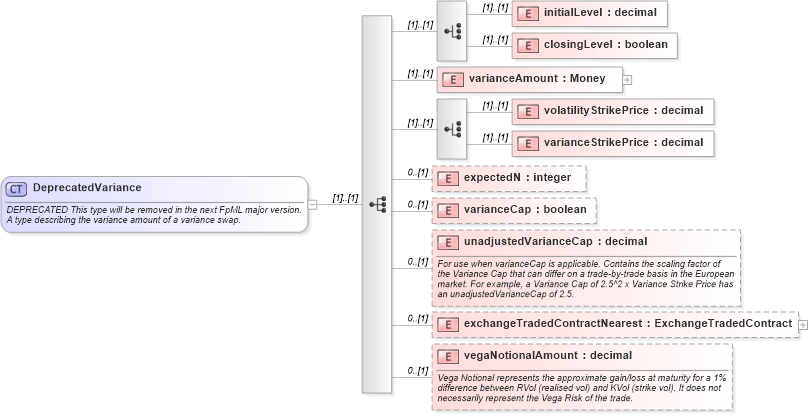

<xsd:documentation xml:lang="en">DEPRECATED This type will be removed in the next FpML major version. A type describing the variance amount of a variance swap.</xsd:documentation>

</xsd:annotation>

<xsd:sequence>

<xsd:choice>

<xsd:element name="initialLevel" type="xsd:decimal" />

<xsd:element name="closingLevel" type="xsd:boolean" />

</xsd:choice>

<xsd:element name="varianceAmount" type="Money" />

<xsd:choice>

<xsd:element name="volatilityStrikePrice" type="xsd:decimal" />

<xsd:element name="varianceStrikePrice" type="xsd:decimal" />

</xsd:choice>

<xsd:element name="expectedN" type="xsd:integer" minOccurs="0" />

<xsd:element name="varianceCap" type="xsd:boolean" minOccurs="0" />

<xsd:element name="unadjustedVarianceCap" type="xsd:decimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">For use when varianceCap is applicable. Contains the scaling factor of the Variance Cap that can differ on a trade-by-trade basis in the European market. For example, a Variance Cap of 2.5^2 x Variance Strike Price has an unadjustedVarianceCap of 2.5.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="exchangeTradedContractNearest" type="ExchangeTradedContract" minOccurs="0" />

<xsd:element name="vegaNotionalAmount" type="xsd:decimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Vega Notional represents the approximate gain/loss at maturity for a 1% difference between RVol (realised vol) and KVol (strike vol). It does not necessarily represent the Vega Risk of the trade.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:complexType>

|