<xsd:complexType name="CommodityOption">

<xsd:annotation>

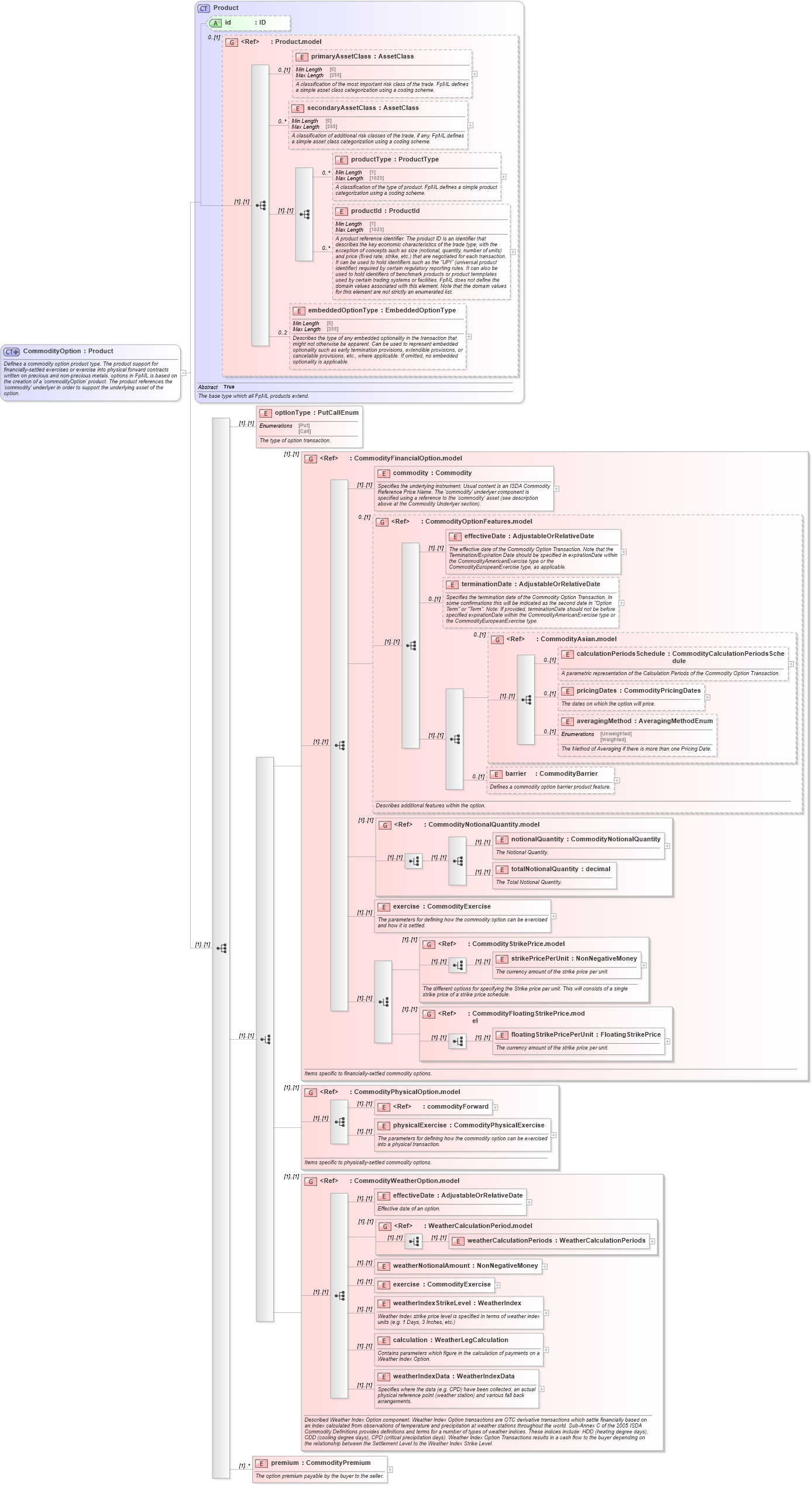

<xsd:documentation xml:lang="en">Defines a commodity option product type. The product support for financially-settled exercises or exercise into physical forward contracts written on precious and non-precious metals. options in FpML is based on the creation of a 'commodityOption' product. The product references the 'commodity' underlyer in order to support the underlying asset of the option.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="Product">

<xsd:sequence>

<xsd:element name="optionType" type="PutCallEnum">

<xsd:annotation>

<xsd:documentation xml:lang="en">The type of option transaction.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:choice>

<xsd:group ref="CommodityFinancialOption.model">

<xsd:annotation>

<xsd:documentation xml:lang="en">Items specific to financially-settled commodity options.</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:group ref="CommodityPhysicalOption.model">

<xsd:annotation>

<xsd:documentation xml:lang="en">Items specific to physically-settled commodity options.</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:group ref="CommodityWeatherOption.model">

<xsd:annotation>

<xsd:documentation xml:lang="en">Described Weather Index Option component. Weather Index Option transactions are OTC derivative transactions which settle financially based on an index calculated from observations of temperature and precipitation at weather stations throughout the world. Sub-Annex C of the 2005 ISDA Commodity Definitions provides definitions and terms for a number of types of weather indices. These indices include: HDD (heating degree days), CDD (cooling degree days), CPD (critical precipitation days). Weather Index Option Transactions results in a cash flow to the buyer depending on the relationship between the Settlement Level to the Weather Index Strike Level.</xsd:documentation>

</xsd:annotation>

</xsd:group>

</xsd:choice>

<xsd:element name="premium" type="CommodityPremium" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">The option premium payable by the buyer to the seller.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|