<xsd:element name="creditDefaultSwap" type="CreditDefaultSwap" substitutionGroup="product">

<xsd:annotation>

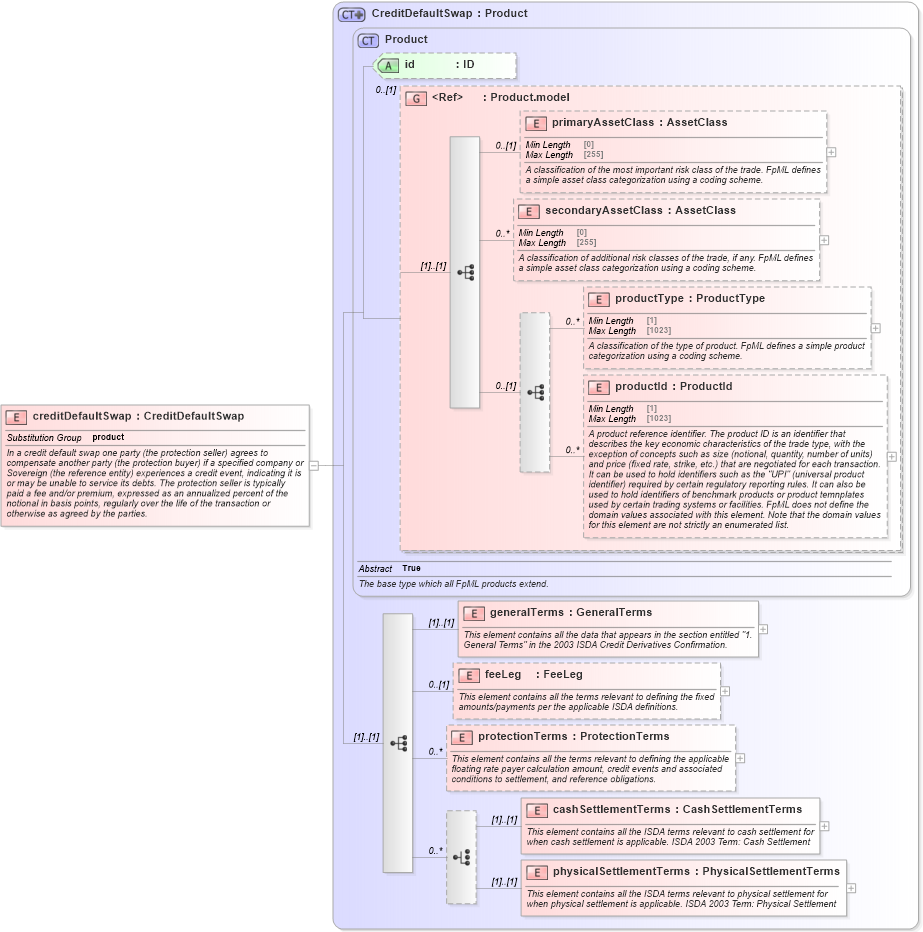

<xsd:documentation xml:lang="en">In a credit default swap one party (the protection seller) agrees to compensate another party (the protection buyer) if a specified company or Sovereign (the reference entity) experiences a credit event, indicating it is or may be unable to service its debts. The protection seller is typically paid a fee and/or premium, expressed as an annualized percent of the notional in basis points, regularly over the life of the transaction or otherwise as agreed by the parties.</xsd:documentation>

</xsd:annotation>

</xsd:element>

|