<xsd:complexType name="ReturnSwapLegUnderlyer" abstract="true">

<xsd:annotation>

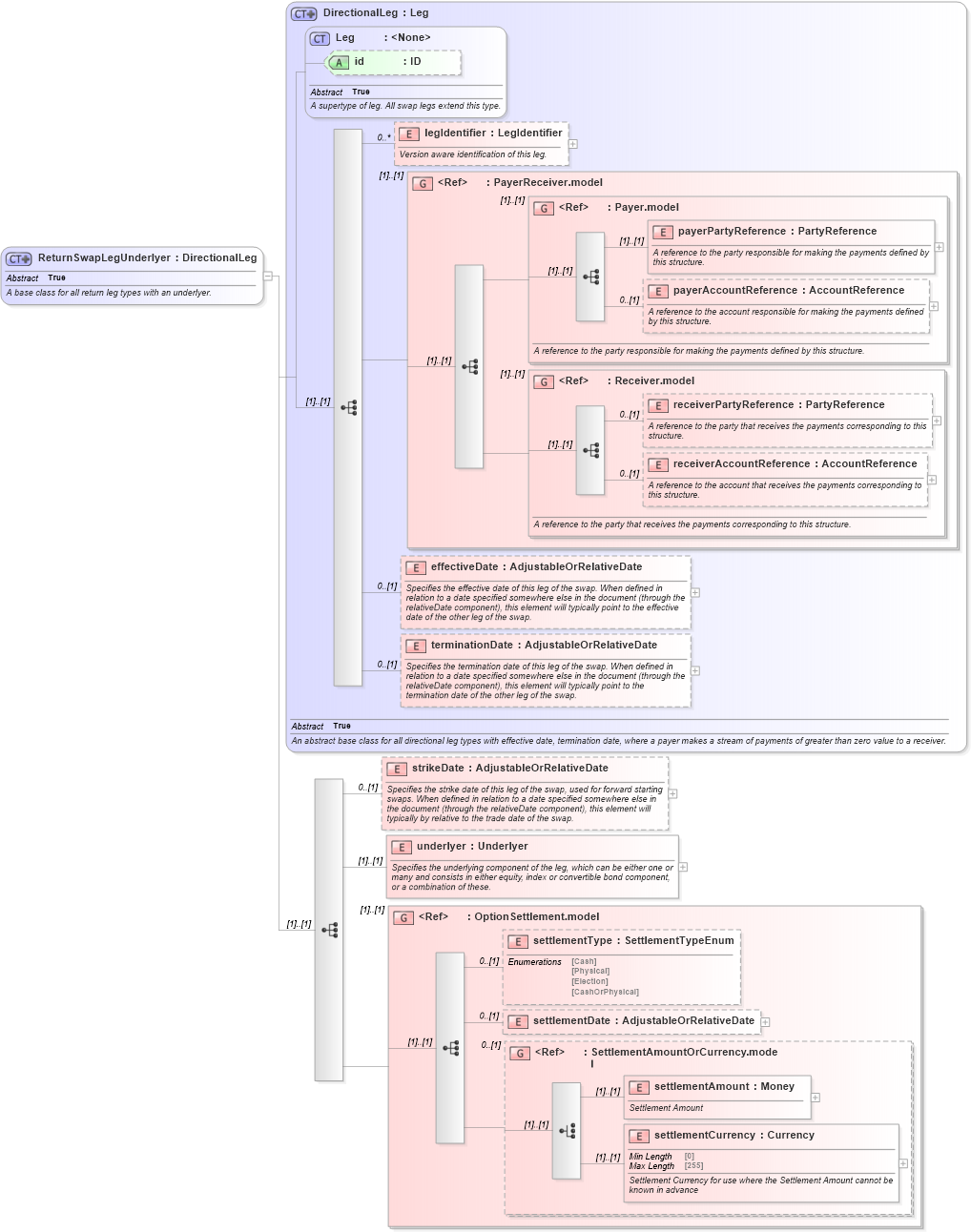

<xsd:documentation xml:lang="en">A base class for all return leg types with an underlyer.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="DirectionalLeg">

<xsd:sequence>

<xsd:element name="strikeDate" type="AdjustableOrRelativeDate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the strike date of this leg of the swap, used for forward starting swaps. When defined in relation to a date specified somewhere else in the document (through the relativeDate component), this element will typically by relative to the trade date of the swap.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="underlyer" type="Underlyer">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the underlying component of the leg, which can be either one or many and consists in either equity, index or convertible bond component, or a combination of these.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:group ref="OptionSettlement.model" />

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|