<xsd:complexType name="Price">

<xsd:annotation>

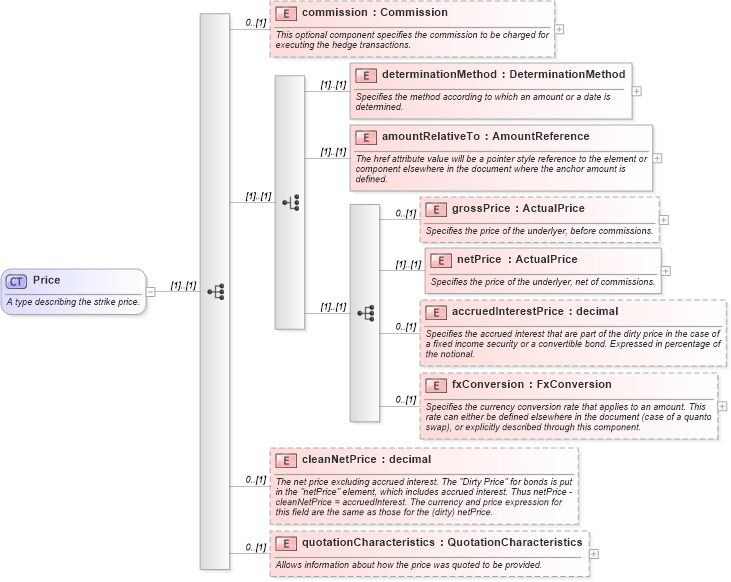

<xsd:documentation xml:lang="en">A type describing the strike price.</xsd:documentation>

</xsd:annotation>

<xsd:sequence>

<xsd:element name="commission" type="Commission" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">This optional component specifies the commission to be charged for executing the hedge transactions.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:choice>

<xsd:element name="determinationMethod" type="DeterminationMethod">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the method according to which an amount or a date is determined.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="amountRelativeTo" type="AmountReference">

<xsd:annotation>

<xsd:documentation xml:lang="en">The href attribute value will be a pointer style reference to the element or component elsewhere in the document where the anchor amount is defined.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:sequence>

<xsd:element name="grossPrice" type="ActualPrice" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the price of the underlyer, before commissions.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="netPrice" type="ActualPrice">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the price of the underlyer, net of commissions.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="accruedInterestPrice" type="xsd:decimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the accrued interest that are part of the dirty price in the case of a fixed income security or a convertible bond. Expressed in percentage of the notional.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="fxConversion" type="FxConversion" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the currency conversion rate that applies to an amount. This rate can either be defined elsewhere in the document (case of a quanto swap), or explicitly described through this component.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:choice>

<xsd:element name="cleanNetPrice" type="xsd:decimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The net price excluding accrued interest. The "Dirty Price" for bonds is put in the "netPrice" element, which includes accrued interest. Thus netPrice - cleanNetPrice = accruedInterest. The currency and price expression for this field are the same as those for the (dirty) netPrice.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="quotationCharacteristics" type="QuotationCharacteristics" minOccurs="0">

<xsd:annotation>

<xsd:documentation>Allows information about how the price was quoted to be provided.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:complexType>

|