<xsd:complexType name="FxAccrualOption">

<xsd:annotation>

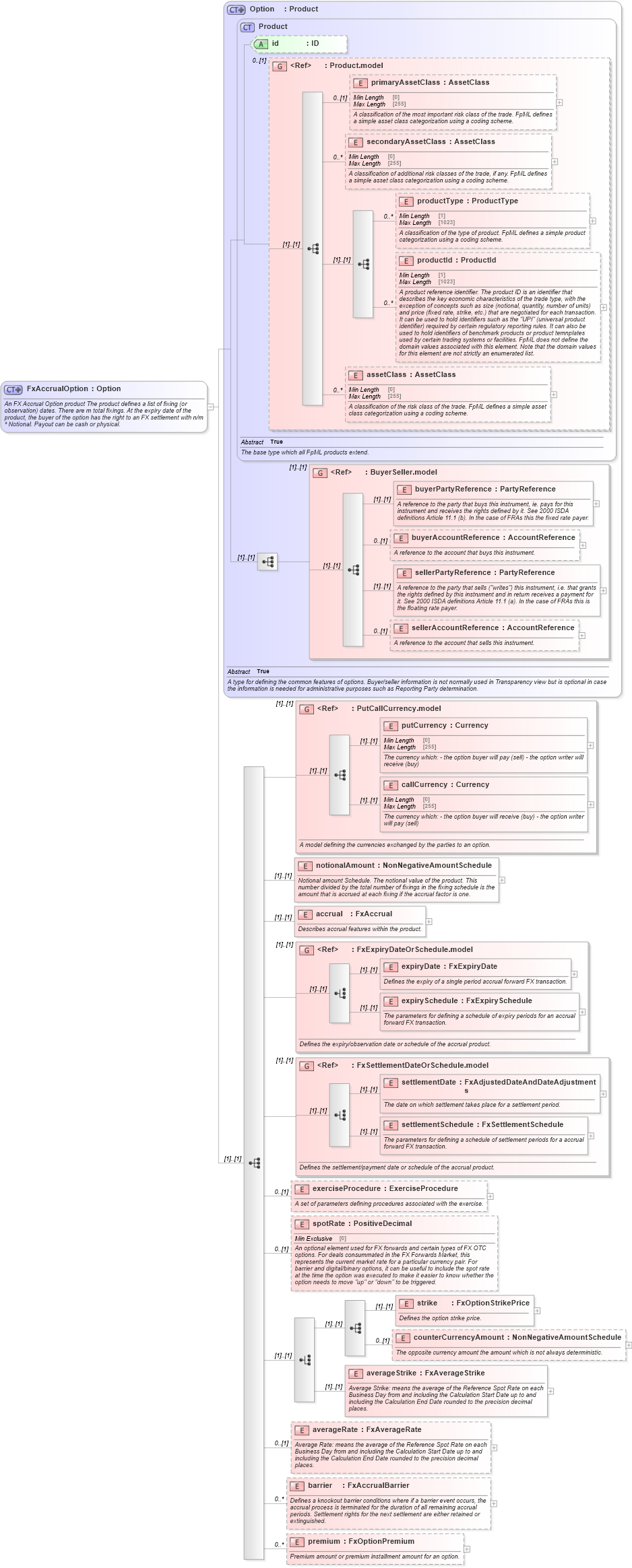

<xsd:documentation xml:lang="en">An FX Accrual Option product The product defines a list of fixing (or observation) dates. There are m total fixings. At the expiry date of the product, the buyer of the option has the right to an FX settlement with n/m * Notional. Payout can be cash or physical.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="Option">

<xsd:sequence>

<xsd:group ref="PutCallCurrency.model">

<xsd:annotation>

<xsd:documentation xml:lang="en">A model defining the currencies exchanged by the parties to an option.</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:element name="notionalAmount" type="NonNegativeAmountSchedule">

<xsd:annotation>

<xsd:documentation xml:lang="en">Notional amount Schedule. The notional value of the product. This number divided by the total number of fixings in the fixing schedule is the amount that is accrued at each fixing if the accrual factor is one.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="accrual" type="FxAccrual">

<xsd:annotation>

<xsd:documentation xml:lang="en">Describes accrual features within the product.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:group ref="FxExpiryDateOrSchedule.model">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the expiry/observation date or schedule of the accrual product.</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:group ref="FxSettlementDateOrSchedule.model">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the settlement/payment date or schedule of the accrual product.</xsd:documentation>

</xsd:annotation>

</xsd:group>

<xsd:element name="exerciseProcedure" type="ExerciseProcedure" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">A set of parameters defining procedures associated with the exercise.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="spotRate" type="PositiveDecimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">An optional element used for FX forwards and certain types of FX OTC options. For deals consummated in the FX Forwards Market, this represents the current market rate for a particular currency pair. For barrier and digital/binary options, it can be useful to include the spot rate at the time the option was executed to make it easier to know whether the option needs to move "up" or "down" to be triggered.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:choice>

<xsd:sequence>

<xsd:element name="strike" type="FxOptionStrikePrice">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the option strike price.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="counterCurrencyAmount" type="NonNegativeAmountSchedule" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">The opposite currency amount the amount which is not always deterministic.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

<xsd:element name="averageStrike" type="FxAverageStrike">

<xsd:annotation>

<xsd:documentation xml:lang="en">Average Strike: means the average of the Reference Spot Rate on each Business Day from and including the Calculation Start Date up to and including the Calculation End Date rounded to the precision decimal places.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:choice>

<xsd:element name="averageRate" type="FxAverageRate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Average Rate: means the average of the Reference Spot Rate on each Business Day from and including the Calculation Start Date up to and including the Calculation End Date rounded to the precision decimal places.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="barrier" type="FxAccrualBarrier" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines a knockout barrier conditions where if a barrier event occurs, the accrual process is terminated for the duration of all remaining accrual periods. Settlement rights for the next settlement are either retained or extinguished.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="premium" type="FxOptionPremium" minOccurs="0" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">Premium amount or premium installment amount for an option.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|