<xsd:complexType name="FxOption">

<xsd:annotation>

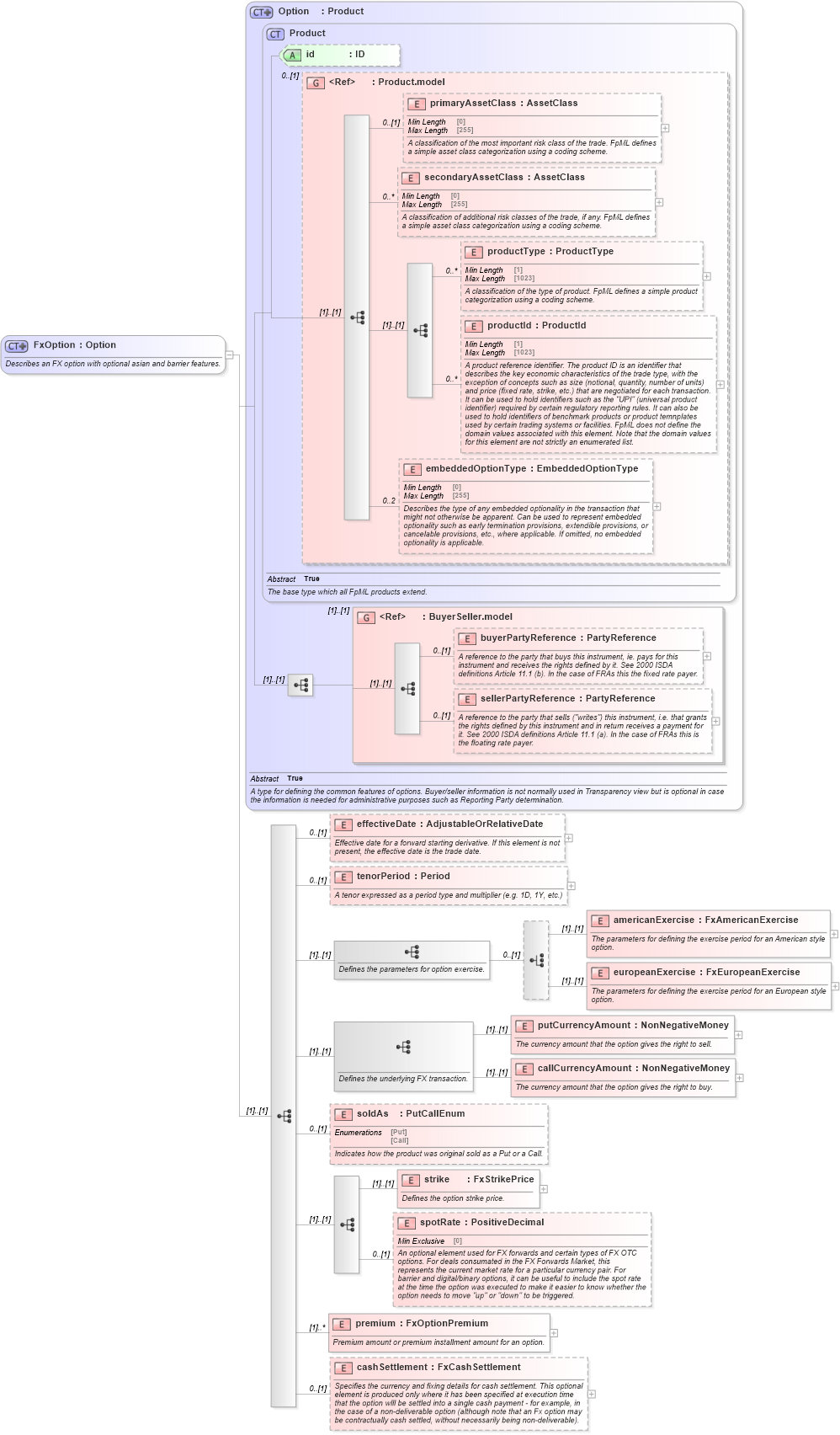

<xsd:documentation xml:lang="en">Describes an FX option with optional asian and barrier features.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="Option">

<xsd:sequence>

<xsd:element name="effectiveDate" type="AdjustableOrRelativeDate" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Effective date for a forward starting derivative. If this element is not present, the effective date is the trade date.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="tenorPeriod" type="Period" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">A tenor expressed as a period type and multiplier (e.g. 1D, 1Y, etc.)</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:sequence>

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the parameters for option exercise.</xsd:documentation>

</xsd:annotation>

<xsd:choice minOccurs="0">

<xsd:element name="americanExercise" type="FxAmericanExercise">

<xsd:annotation>

<xsd:documentation xml:lang="en">The parameters for defining the exercise period for an American style option.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="europeanExercise" type="FxEuropeanExercise">

<xsd:annotation>

<xsd:documentation xml:lang="en">The parameters for defining the exercise period for an European style option.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:choice>

</xsd:sequence>

<xsd:sequence>

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the underlying FX transaction.</xsd:documentation>

</xsd:annotation>

<xsd:element name="putCurrencyAmount" type="NonNegativeMoney">

<xsd:annotation>

<xsd:documentation xml:lang="en">The currency amount that the option gives the right to sell.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="callCurrencyAmount" type="NonNegativeMoney">

<xsd:annotation>

<xsd:documentation xml:lang="en">The currency amount that the option gives the right to buy.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

<xsd:element name="soldAs" type="PutCallEnum" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Indicates how the product was original sold as a Put or a Call.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:sequence>

<xsd:element name="strike" type="FxStrikePrice">

<xsd:annotation>

<xsd:documentation xml:lang="en">Defines the option strike price.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="spotRate" type="PositiveDecimal" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">An optional element used for FX forwards and certain types of FX OTC options. For deals consumated in the FX Forwards Market, this represents the current market rate for a particular currency pair. For barrier and digital/binary options, it can be useful to include the spot rate at the time the option was executed to make it easier to know whether the option needs to move "up" or "down" to be triggered.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

<xsd:element name="premium" type="FxOptionPremium" maxOccurs="unbounded">

<xsd:annotation>

<xsd:documentation xml:lang="en">Premium amount or premium installment amount for an option.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="cashSettlement" type="FxCashSettlement" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the currency and fixing details for cash settlement. This optional element is produced only where it has been specified at execution time that the option wlll be settled into a single cash payment - for example, in the case of a non-deliverable option (although note that an Fx option may be contractually cash settled, without necessarily being non-deliverable).</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|