<xsd:complexType name="InterestLeg">

<xsd:annotation>

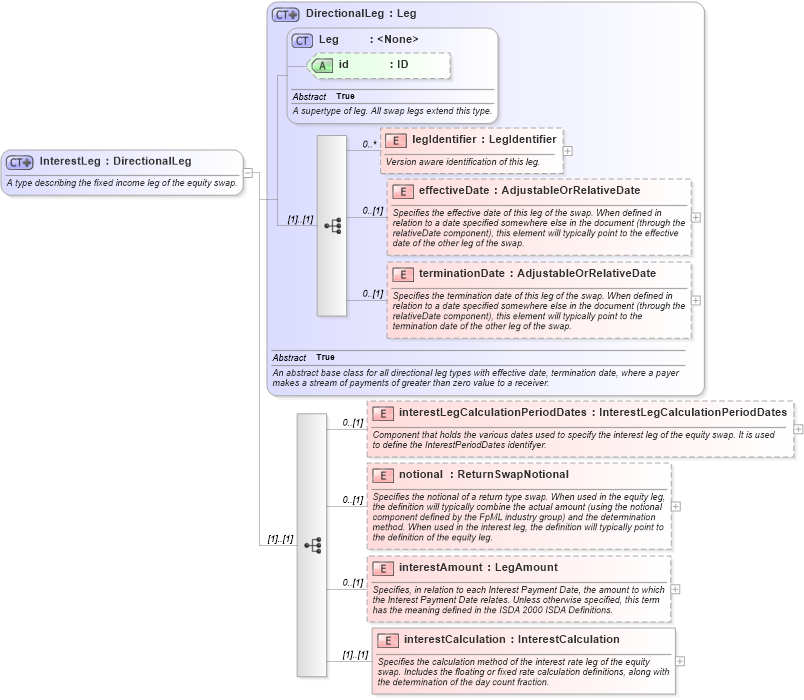

<xsd:documentation xml:lang="en">A type describing the fixed income leg of the equity swap.</xsd:documentation>

</xsd:annotation>

<xsd:complexContent>

<xsd:extension base="DirectionalLeg">

<xsd:sequence>

<xsd:element name="interestLegCalculationPeriodDates" type="InterestLegCalculationPeriodDates" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Component that holds the various dates used to specify the interest leg of the equity swap. It is used to define the InterestPeriodDates identifyer.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="notional" type="ReturnSwapNotional" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the notional of a return type swap. When used in the equity leg, the definition will typically combine the actual amount (using the notional component defined by the FpML industry group) and the determination method. When used in the interest leg, the definition will typically point to the definition of the equity leg.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="interestAmount" type="LegAmount" minOccurs="0">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies, in relation to each Interest Payment Date, the amount to which the Interest Payment Date relates. Unless otherwise specified, this term has the meaning defined in the ISDA 2000 ISDA Definitions.</xsd:documentation>

</xsd:annotation>

</xsd:element>

<xsd:element name="interestCalculation" type="InterestCalculation">

<xsd:annotation>

<xsd:documentation xml:lang="en">Specifies the calculation method of the interest rate leg of the equity swap. Includes the floating or fixed rate calculation definitions, along with the determination of the day count fraction.</xsd:documentation>

</xsd:annotation>

</xsd:element>

</xsd:sequence>

</xsd:extension>

</xsd:complexContent>

</xsd:complexType>

|